Since October 2025, Lowe's has been in a holding pattern, floating around $244.89.

Is there a buying opportunity in Lowe's, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Lowe's Not Exciting?

We're sitting this one out for now. Here are three reasons there are better opportunities than LOW and a stock we'd rather own.

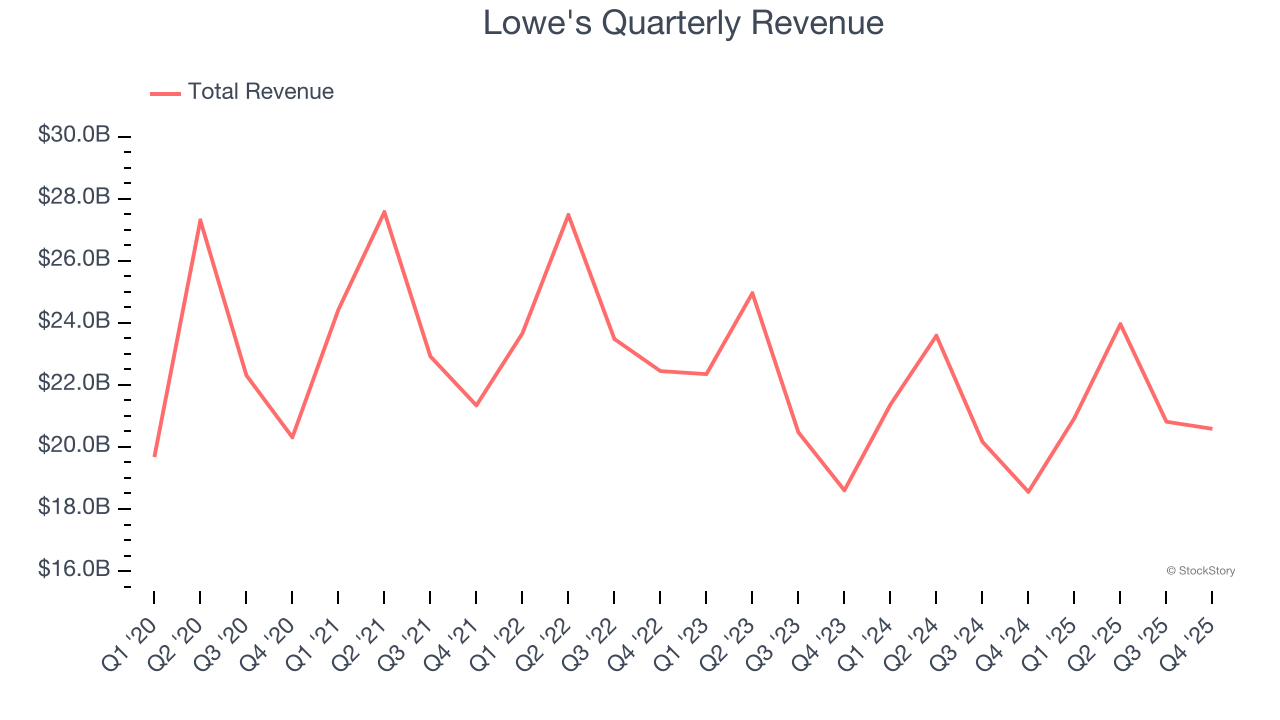

1. Revenue Spiraling Downwards

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Lowe's struggled to consistently generate demand over the last three years as its sales dropped at a 3.8% annual rate. This wasn’t a great result and signals it’s a lower quality business.

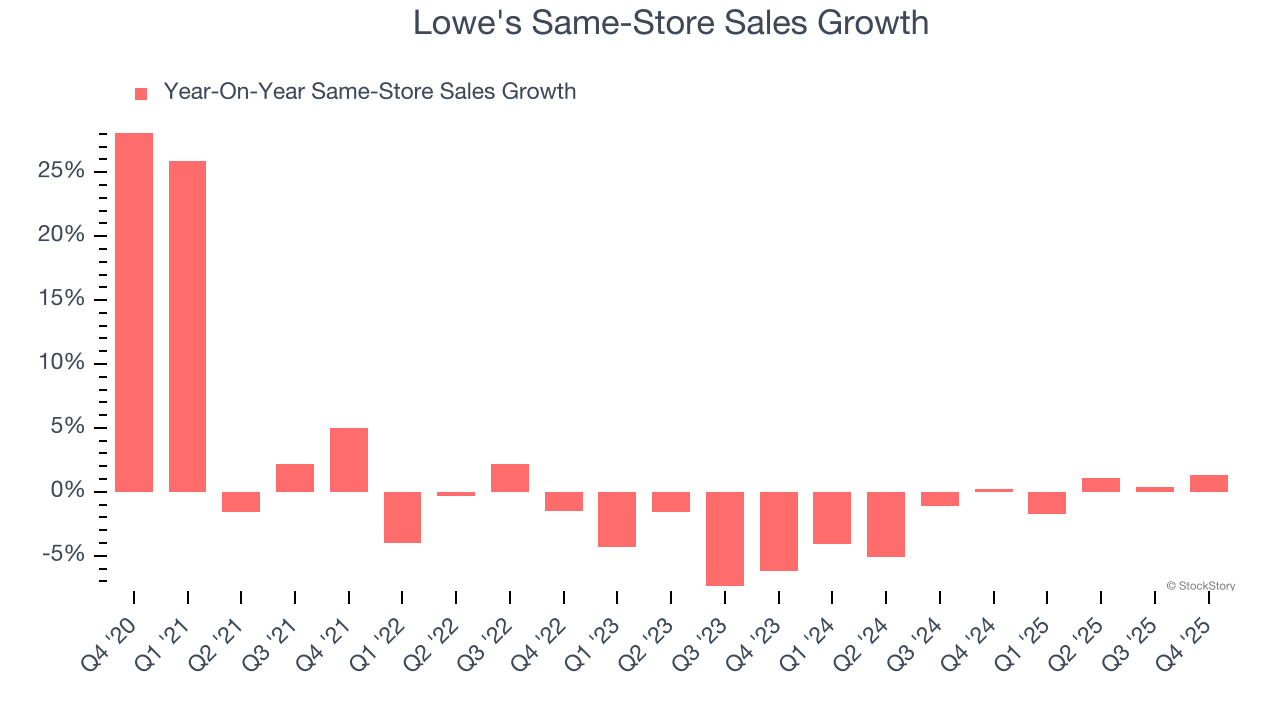

2. Shrinking Same-Store Sales Indicate Waning Demand

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Lowe’s demand has been shrinking over the last two years as its same-store sales have averaged 1.1% annual declines.

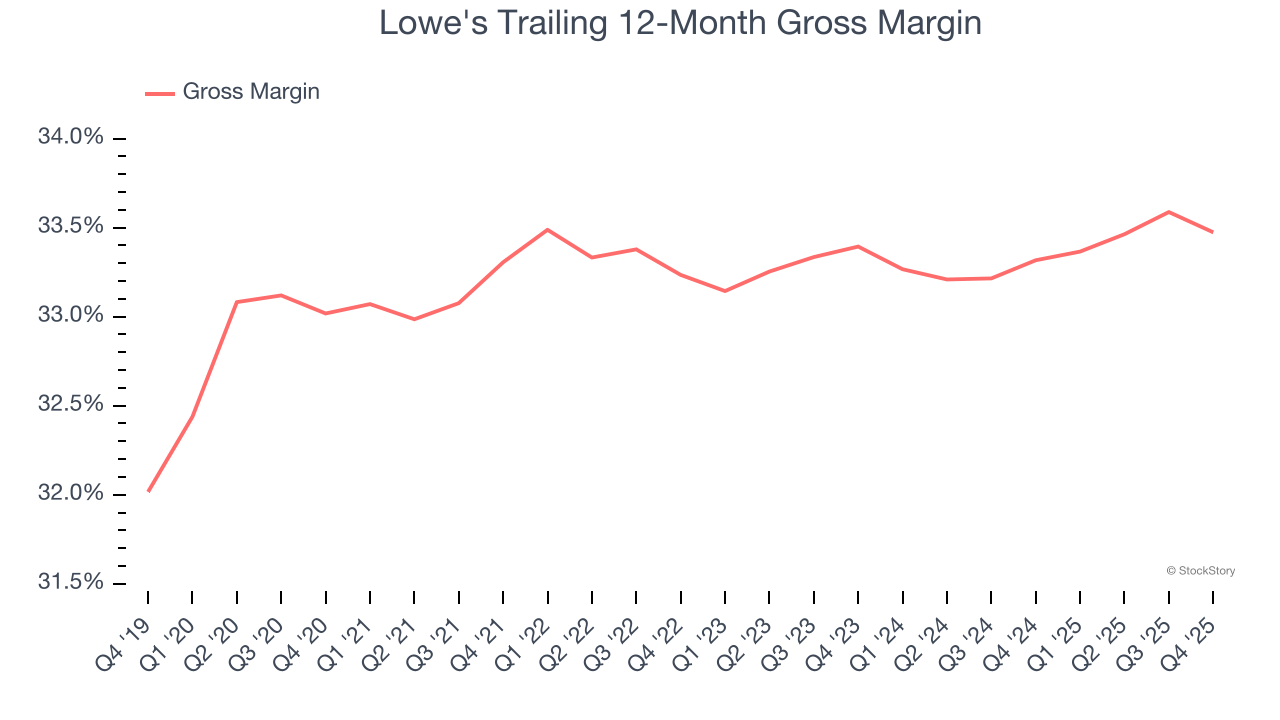

3. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

Lowe's has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 33.4% gross margin over the last two years. Said differently, Lowe's had to pay a chunky $66.60 to its suppliers for every $100 in revenue.

Final Judgment

Lowe's isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 19.9× forward P/E (or $244.89 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of Lowe's

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.