Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Roku (NASDAQ: ROKU) and the best and worst performers in the consumer subscription industry.

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

The 8 consumer subscription stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 1.7% while next quarter’s revenue guidance was 2.1% above.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

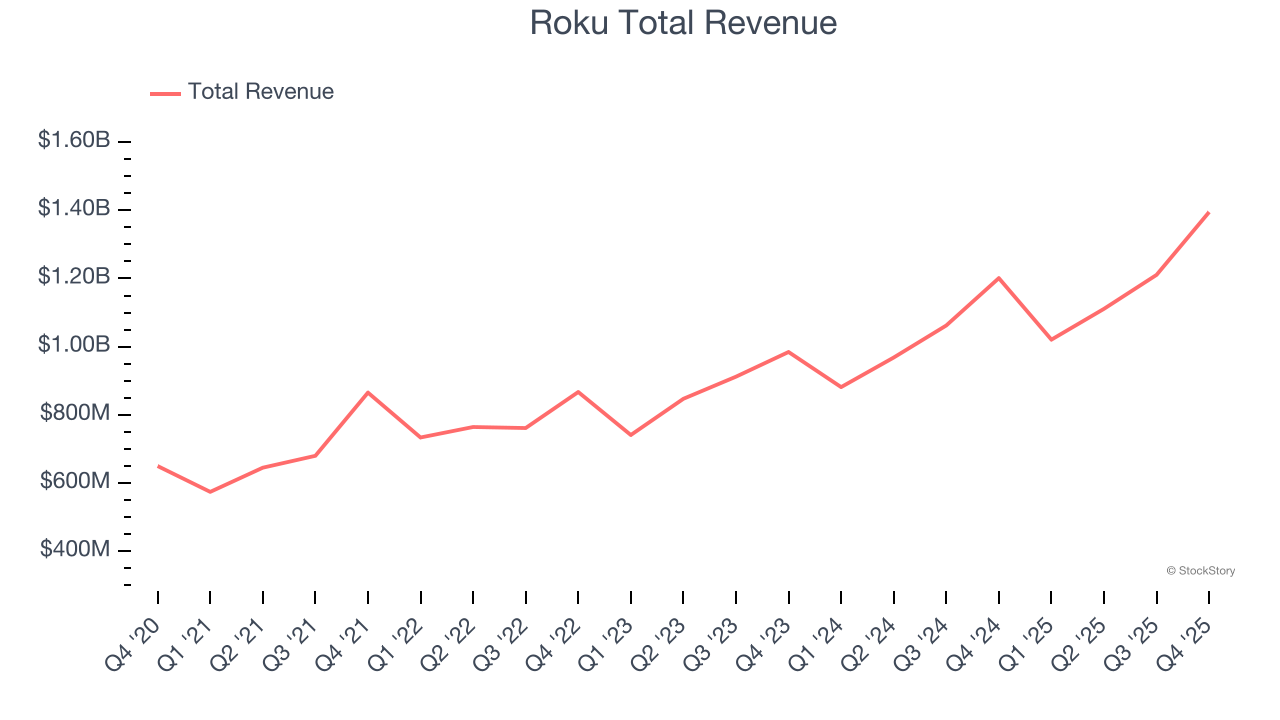

Best Q4: Roku (NASDAQ: ROKU)

With a name meaning six in Japanese because it was the founder's sixth company that he started, Roku (NASDAQ: ROKU) makes hardware players that offer access to various online streaming TV services.

Roku reported revenues of $1.39 billion, up 16.1% year on year. This print exceeded analysts’ expectations by 3%. Overall, it was an exceptional quarter for the company with EBITDA guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ EBITDA estimates.

Roku achieved the biggest analyst estimates beat of the whole group. Unsurprisingly, the stock is up 6% since reporting and currently trades at $87.87.

We think Roku is a good business, but is it a buy today? Read our full report here, it’s free.

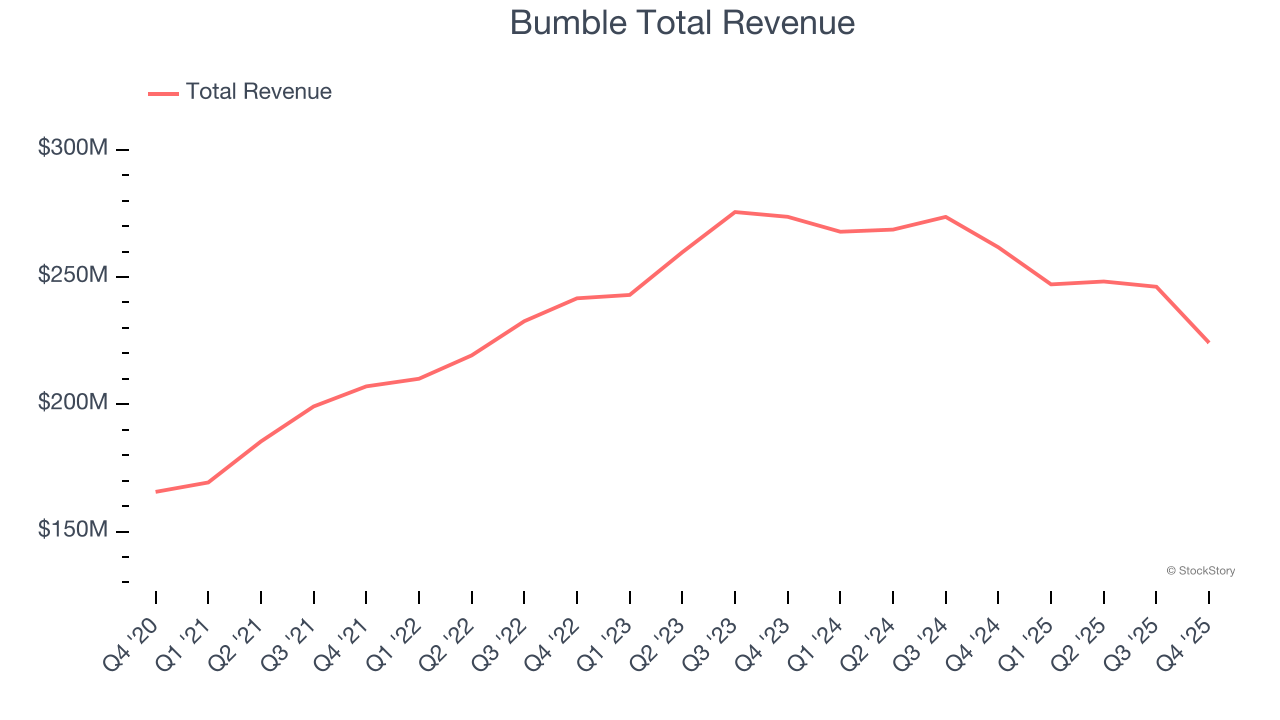

Bumble (NASDAQ: BMBL)

Started by the co-founder of Tinder, Whitney Wolfe Herd, Bumble (NASDAQ: BMBL) is a leading dating app built with women at the center.

Bumble reported revenues of $224.2 million, down 14.3% year on year, outperforming analysts’ expectations by 1.2%. The business had an exceptional quarter with EBITDA guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 15.1% since reporting. It currently trades at $3.27.

Is now the time to buy Bumble? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Duolingo (NASDAQ: DUOL)

Founded by a Carnegie Mellon computer science professor and his Ph.D. student, Duolingo (NASDAQ: DUOL) is a mobile app helping people learn new languages.

Duolingo reported revenues of $282.9 million, up 35% year on year, exceeding analysts’ expectations by 2.5%. Still, it was a softer quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and full-year EBITDA guidance missing analysts’ expectations significantly.

As expected, the stock is down 20.1% since the results and currently trades at $93.88.

Read our full analysis of Duolingo’s results here.

Netflix (NASDAQ: NFLX)

Launched by Reed Hastings as a DVD mail rental company until its famous pivot to streaming in 2007, Netflix (NASDAQ: NFLX) is a pioneering streaming content platform.

Netflix reported revenues of $12.05 billion, up 17.6% year on year. This print surpassed analysts’ expectations by 0.7%. However, it was a slower quarter as it recorded EPS guidance for next quarter missing analysts’ expectations and revenue guidance for next quarter meeting analysts’ expectations.

Netflix scored the highest full-year guidance raise among its peers. The stock is up 6.2% since reporting and currently trades at $92.68.

Read our full, actionable report on Netflix here, it’s free.

Match Group (NASDAQ: MTCH)

Originally started as a dial-up service before widespread internet adoption, Match (NASDAQ: MTCH) was an early innovator in online dating and today has a portfolio of apps including Tinder, Hinge, Archer, and OkCupid.

Match Group reported revenues of $878 million, up 2.1% year on year. This number topped analysts’ expectations by 0.7%. More broadly, it was a mixed quarter as it also recorded EBITDA guidance for next quarter exceeding analysts’ expectations but full-year revenue guidance missing analysts’ expectations significantly.

Match Group had the weakest full-year guidance update among its peers. The company reported 13.84 million users, down 5.2% year on year. The stock is up 4.1% since reporting and currently trades at $30.08.

Read our full, actionable report on Match Group here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.