Let’s dig into the relative performance of Atlanticus Holdings (NASDAQ: ATLC) and its peers as we unravel the now-completed Q4 personal loan earnings season.

Personal loan providers offer unsecured credit for various consumer needs. The sector benefits from digital application processes, increasing consumer comfort with online financial services, and opportunities in underserved credit segments. Headwinds include credit risk management in unsecured lending, regulatory oversight of lending practices, and intense competition affecting margins from both traditional and fintech lenders.

The 9 personal loan stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 2.8% while next quarter’s revenue guidance was 1% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 11.4% since the latest earnings results.

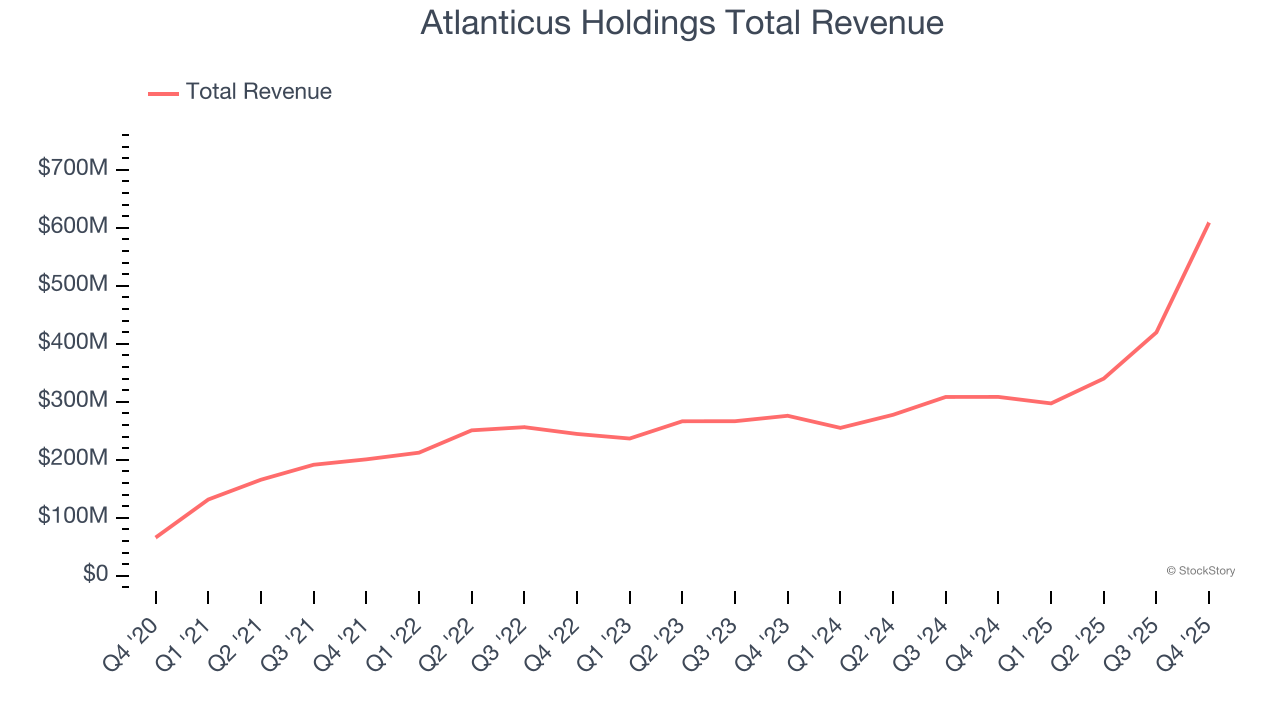

Best Q4: Atlanticus Holdings (NASDAQ: ATLC)

Using data analytics to serve the millions of Americans with less-than-perfect credit scores, Atlanticus Holdings (NASDAQ: ATLC) provides technology and services that help lenders offer credit products to consumers often overlooked by traditional financing providers.

Atlanticus Holdings reported revenues of $609.2 million, up 97.4% year on year. This print exceeded analysts’ expectations by 7.1%. Overall, it was an exceptional quarter for the company with a solid beat of analysts’ revenue and EPS estimates.

Jeff Howard, President and Chief Executive Officer of Atlanticus stated, “We are pleased to have achieved both our return on capital and earnings growth goals in the quarter and for the year. With quarterly Net income attributable to common shareholders increasing approximately 25%, annual Net income attributable to common shareholders growing approximately 28%, all while achieving a return on average equity in excess of 22%, we continue to demonstrate the earnings power of the Atlanticus platform. While our historical lines of business continue to perform within our expectations, we added a significant contributor to long-term earnings growth with the acquisition of Mercury Financial in the third quarter of 2025. I am especially proud of the way our team has come together to integrate the two businesses while continuing to remain focused on the most important driver of shareholder value creation – unit level profitability. The integration of Mercury is ahead of our plan and we are realizing many of the revenue and operating synergies faster and more materially than we had forecasted.

Atlanticus Holdings achieved the biggest analyst estimates beat and fastest revenue growth of the whole group. The results were likely priced in, however, and the stock is flat since reporting. It currently trades at $53.05.

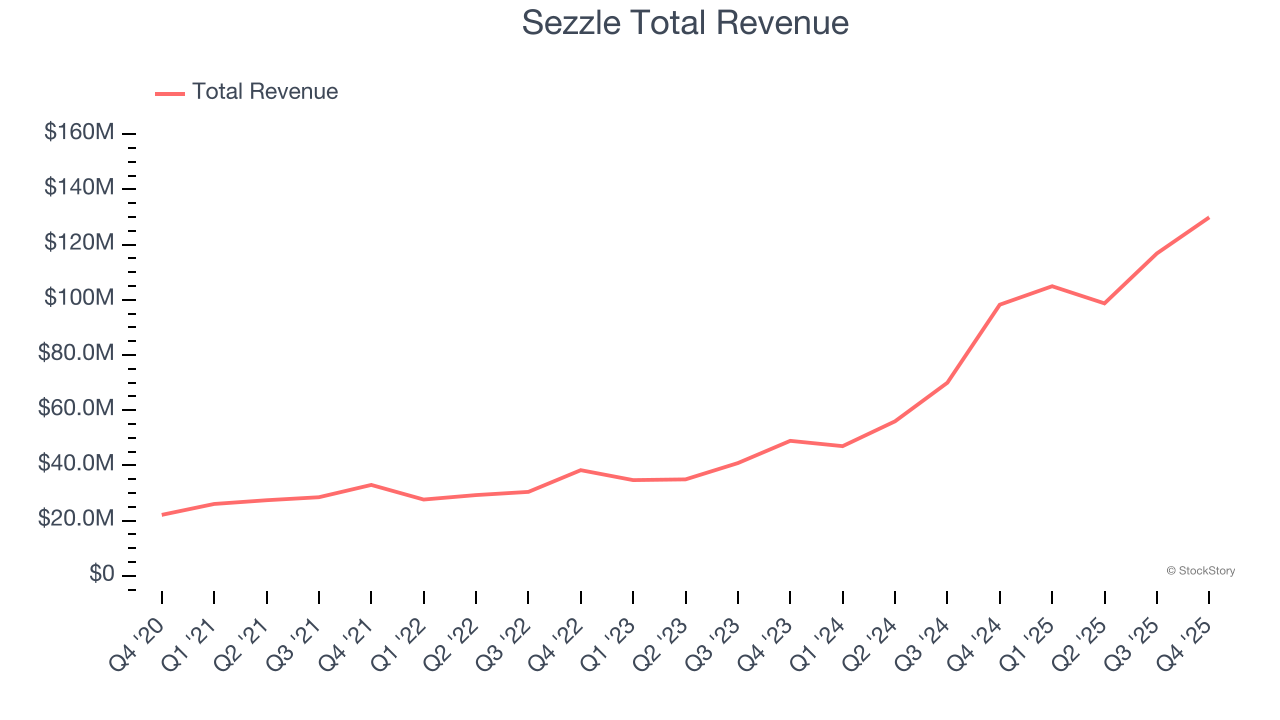

Sezzle (NASDAQ: SEZL)

Founded in 2016 as an alternative to traditional credit cards for younger shoppers, Sezzle (NASDAQ: SEZL) provides a payment platform that allows consumers to split purchases into four interest-free installments over six weeks at participating retailers.

Sezzle reported revenues of $129.9 million, up 32.2% year on year, outperforming analysts’ expectations by 2.7%. The business had an exceptional quarter with a beat of analysts’ EPS and EBITDA estimates.

The market seems content with the results as the stock is up 3.9% since reporting. It currently trades at $65.09.

Is now the time to buy Sezzle? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Affirm (NASDAQ: AFRM)

Founded by PayPal co-founder Max Levchin with a mission to create honest financial products, Affirm (NASDAQ: AFRM) provides a payment network that allows consumers to make purchases and pay for them over time with transparent, flexible installment loans.

Affirm reported revenues of $1.12 billion, up 29.6% year on year, exceeding analysts’ expectations by 6.3%. Still, it was a mixed quarter as it posted a significant miss of analysts’ EPS estimates.

As expected, the stock is down 24.9% since the results and currently trades at $44.63.

Read our full analysis of Affirm’s results here.

LendingClub (NYSE: LC)

Pioneering peer-to-peer lending in the US before evolving into a digital bank, LendingClub (NYSE: LC) operates a marketplace that connects borrowers with lenders, offering personal loans, auto refinancing, and banking services.

LendingClub reported revenues of $266.5 million, up 22.7% year on year. This result topped analysts’ expectations by 1.8%. Overall, it was a strong quarter as it also logged full-year EPS guidance beating analysts’ expectations and a decent beat of analysts’ revenue estimates.

The stock is down 32.3% since reporting and currently trades at $13.26.

Read our full, actionable report on LendingClub here, it’s free.

Dave (NASDAQ: DAVE)

Named after the biblical David fighting financial Goliaths, Dave (NASDAQ: DAVE) is a digital financial services platform that helps Americans living paycheck to paycheck with cash advances, banking services, and tools to improve their financial health.

Dave reported revenues of $163.7 million, up 62.4% year on year. This number beat analysts’ expectations by 0.9%. It was a strong quarter as it also recorded full-year revenue guidance exceeding analysts’ expectations and an impressive beat of analysts’ revenue estimates.

Dave had the weakest full-year guidance update among its peers. The stock is up 3.2% since reporting and currently trades at $205.35.

Read our full, actionable report on Dave here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.