Over the last six months, Lake City Bank’s shares have sunk to $56.73, producing a disappointing 11.3% loss while the S&P 500 was flat. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Lake City Bank, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Lake City Bank Will Underperform?

Even with the cheaper entry price, we're swiping left on Lake City Bank for now. Here are three reasons there are better opportunities than LKFN and a stock we'd rather own.

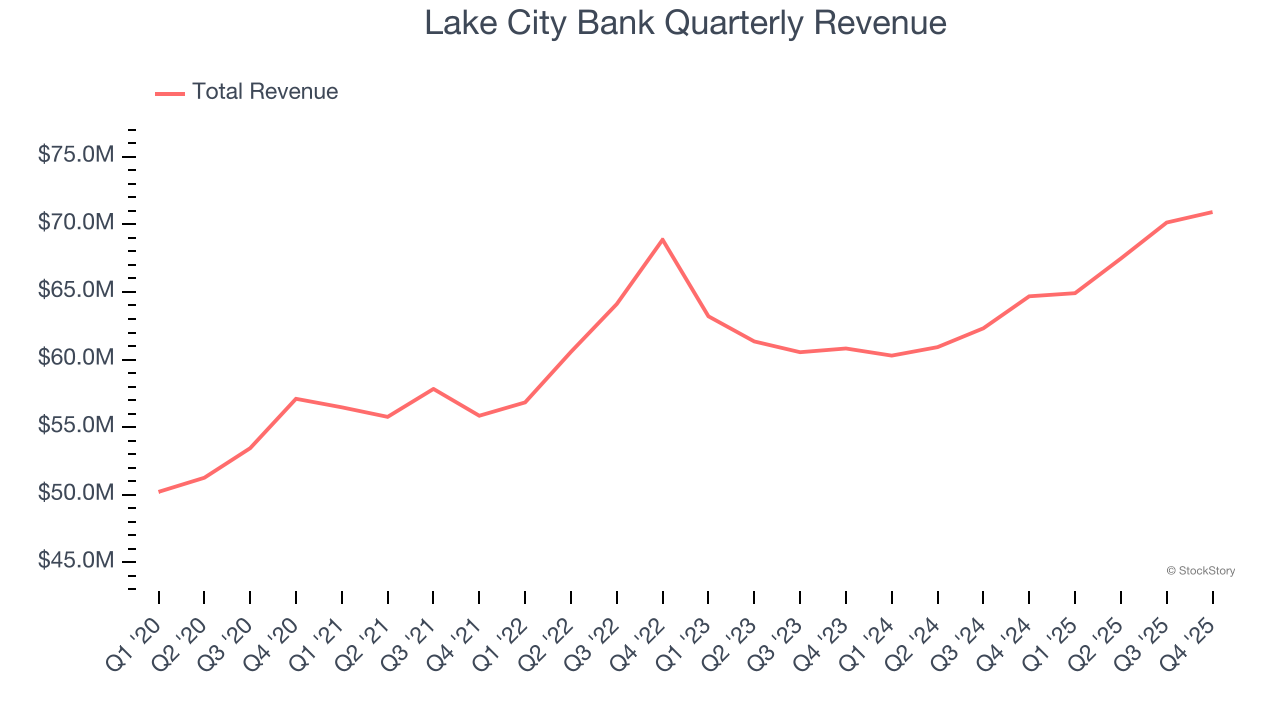

1. Long-Term Revenue Growth Disappoints

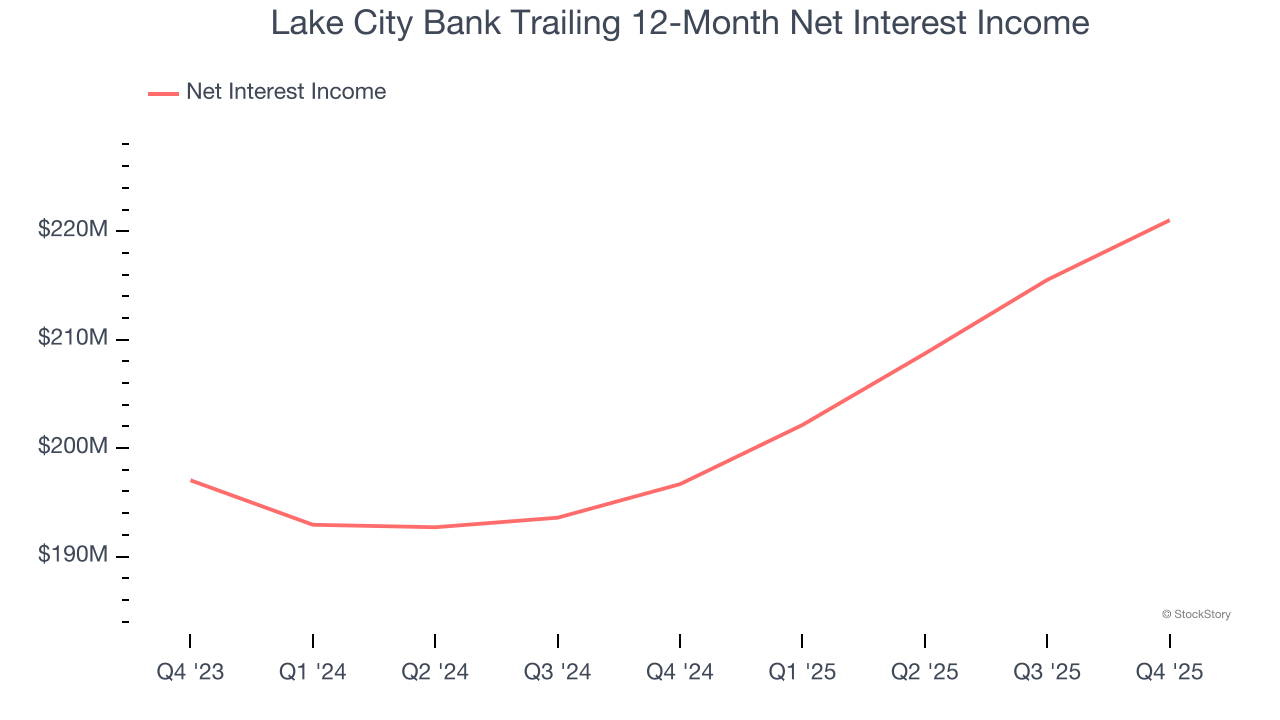

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities.

Over the last five years, Lake City Bank grew its revenue at a sluggish 5.2% compounded annual growth rate. This was below our standard for the banking sector.

2. Net Interest Income Points to Soft Demand

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

Lake City Bank’s net interest income has grown at a 6.3% annualized rate over the last five years, worse than the broader banking industry. Its growth was driven by both an increase in its outstanding loans and net interest margin, which represents how much a bank earns in relation to its outstanding loan book.

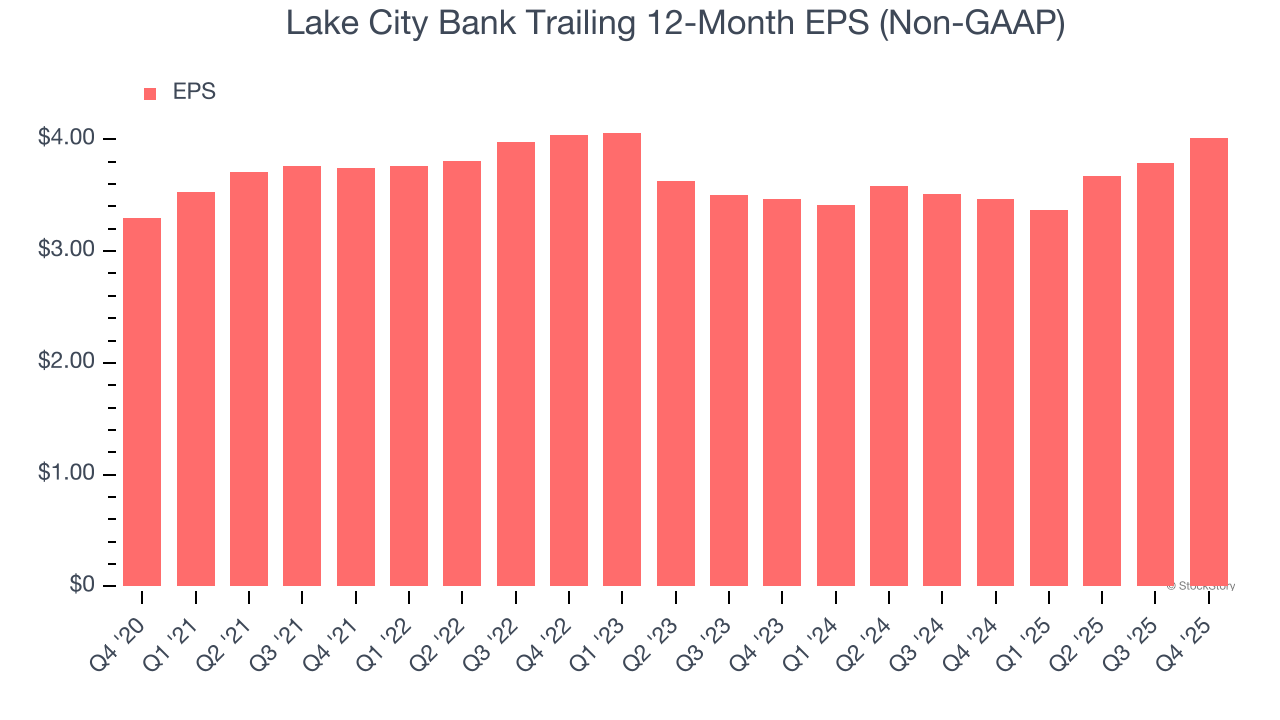

3. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Lake City Bank’s weak 4% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

Final Judgment

Lake City Bank doesn’t pass our quality test. Following the recent decline, the stock trades at 1.7× forward P/B (or $56.73 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Lake City Bank

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.