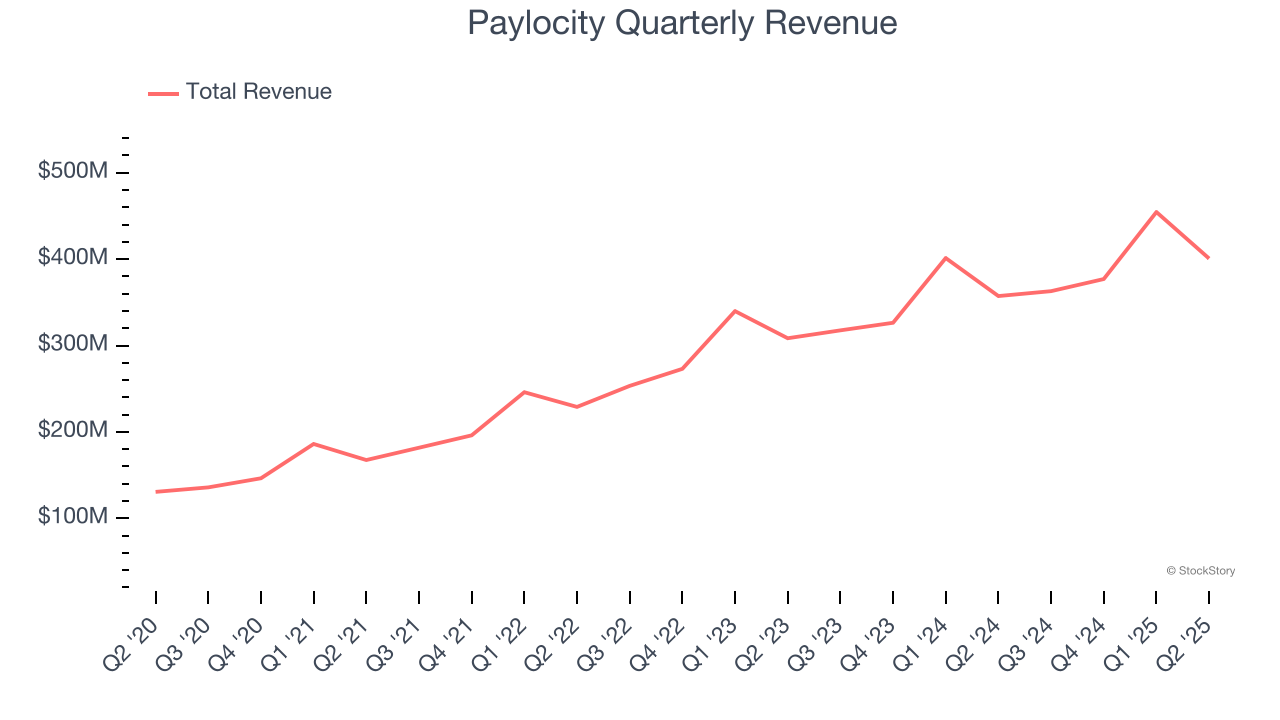

Payroll and human resources software provider, Paylocity (NASDAQ: PCTY) beat Wall Street’s revenue expectations in Q2 CY2025, with sales up 12.2% year on year to $400.7 million. Guidance for next quarter’s revenue was better than expected at $400 million at the midpoint, 2% above analysts’ estimates. Its non-GAAP profit of $1.56 per share was 12.7% above analysts’ consensus estimates.

Is now the time to buy Paylocity? Find out by accessing our full research report, it’s free.

Paylocity (PCTY) Q2 CY2025 Highlights:

- Revenue: $400.7 million vs analyst estimates of $388.6 million (12.2% year-on-year growth, 3.1% beat)

- Adjusted EPS: $1.56 vs analyst estimates of $1.38 (12.7% beat)

- Adjusted Operating Income: $105.6 million vs analyst estimates of $98.31 million (26.4% margin, 7.4% beat)

- Revenue Guidance for Q3 CY2025 is $400 million at the midpoint, above analyst estimates of $392.2 million

- EBITDA guidance for the upcoming financial year 2026 is $613.5 million at the midpoint, in line with analyst expectations

- Operating Margin: 16.5%, down from 17.6% in the same quarter last year

- Free Cash Flow Margin: 16%, down from 36.9% in the previous quarter

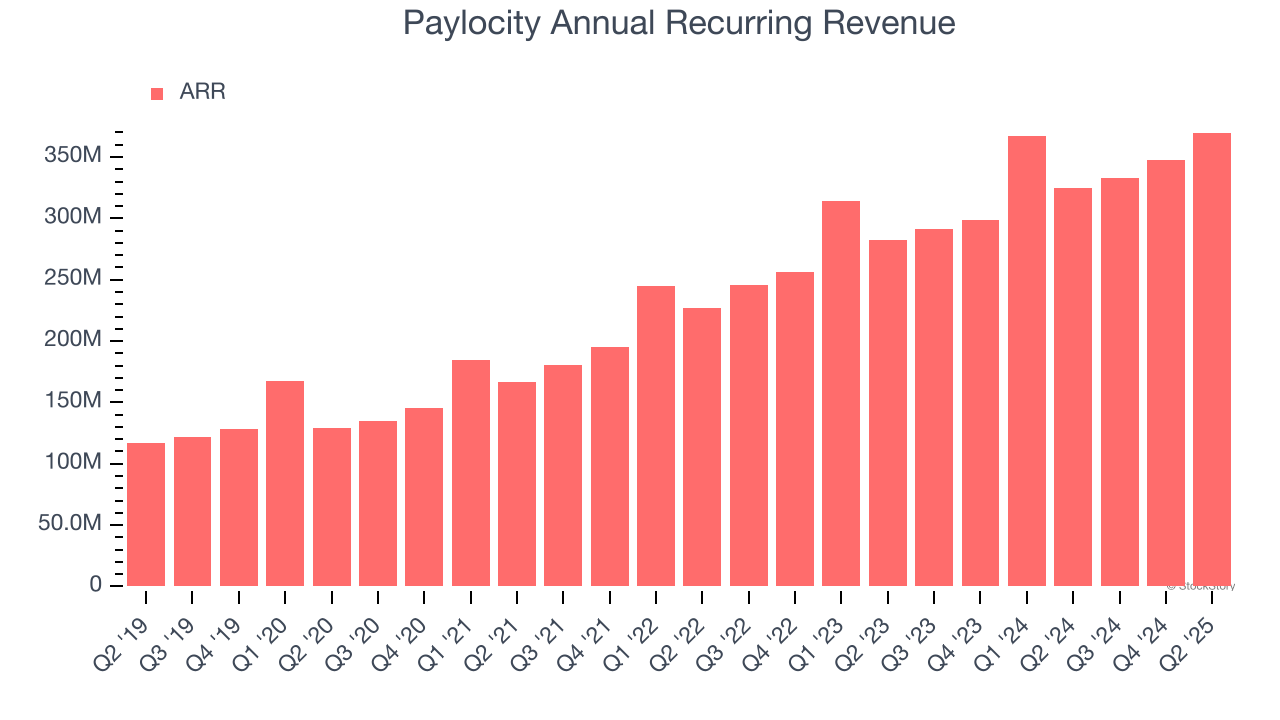

- Annual Recurring Revenue: $369.9 million at quarter end, up 13.9% year on year

- Market Capitalization: $10.14 billion

“Fiscal 25 was a very strong year as our differentiated position in the market was reflected in solid sales and operational execution, helping to drive 15% recurring and other revenue growth and 14% total revenue growth. Our strong growth was driven by the continued expansion of average revenue per client and a 7% increase in our client base – while also focusing on efficiency and productivity across our organization. Most recently, we announced the launch of Paylocity for Finance, expanding our modern workforce platform into the Office of the CFO, and bringing both finance and HR teams together through a unified system grounded in the employee record. By unifying data to connect critical workflows, we’re delivering enhanced visibility, improved efficiency, and an exceptional user experience that drives value through increased adoption across teams. In addition to strong revenue and profitability growth in fiscal 25, we also returned capital to shareholders by repurchasing $150 million or approximately 800,000 shares of our stock. I would also like to thank all of our employees for their efforts supporting our clients, and congratulate our teams for another successful year,” said Toby Williams, President and Chief Executive Officer of Paylocity.

Company Overview

Founded by payroll software veteran Steve Sarowitz in 1997, Paylocity (NASDAQ: PCTY) is a provider of payroll and HR software for small and medium-sized enterprises.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Paylocity’s sales grew at a decent 23.2% compounded annual growth rate over the last three years. Its growth was slightly above the average software company and shows its offerings resonate with customers.

This quarter, Paylocity reported year-on-year revenue growth of 12.2%, and its $400.7 million of revenue exceeded Wall Street’s estimates by 3.1%. Company management is currently guiding for a 10.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7.1% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products and services will face some demand challenges.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Paylocity’s ARR punched in at $369.9 million in Q2, and over the last four quarters, its growth was solid as it averaged 14.9% year-on-year increases. This performance aligned with its total sales growth, reflecting the company’s ability to maintain strong customer relationships and secure longer-term commitments. Its growth also contributes positively to Paylocity’s predictability and valuation, as investors typically prefer businesses with recurring revenue.

Customer Acquisition Efficiency

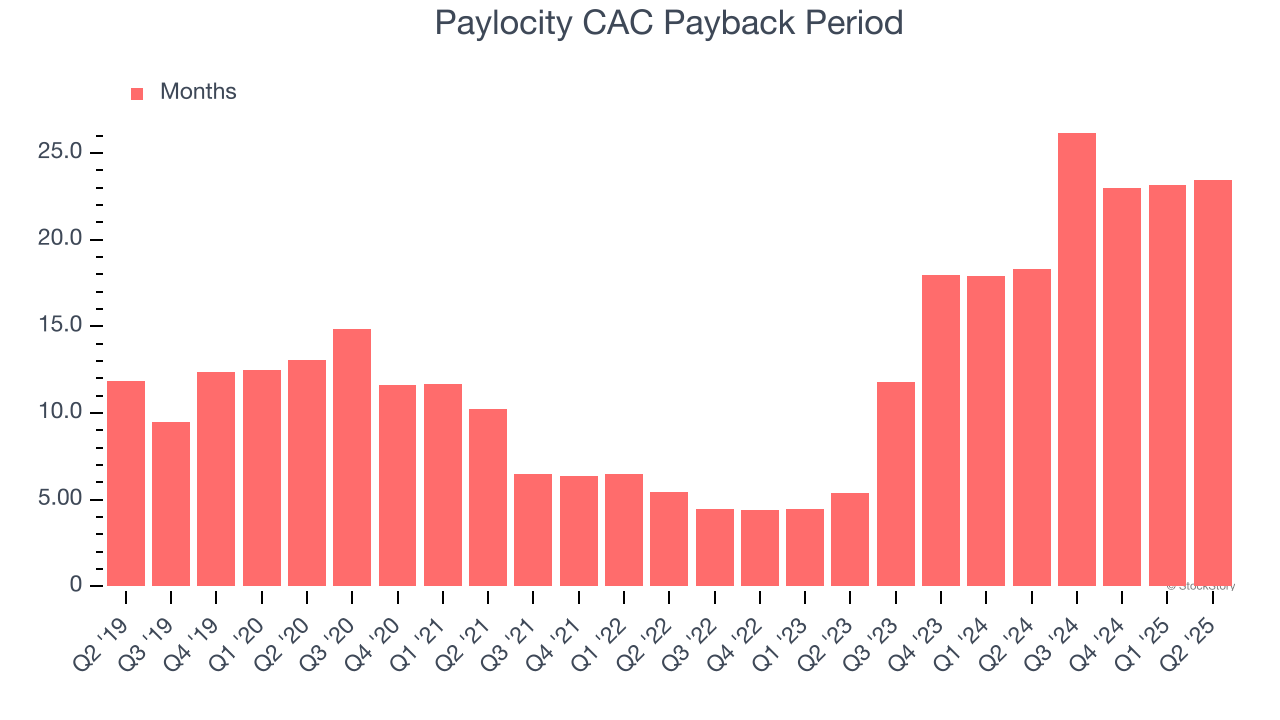

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Paylocity is very efficient at acquiring new customers, and its CAC payback period checked in at 23.4 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Paylocity more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Key Takeaways from Paylocity’s Q2 Results

We were impressed by how significantly Paylocity blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand. Overall, this print had some key positives. The stock traded up 5.7% to $192 immediately following the results.

Paylocity may have had a good quarter, but does that mean you should invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.