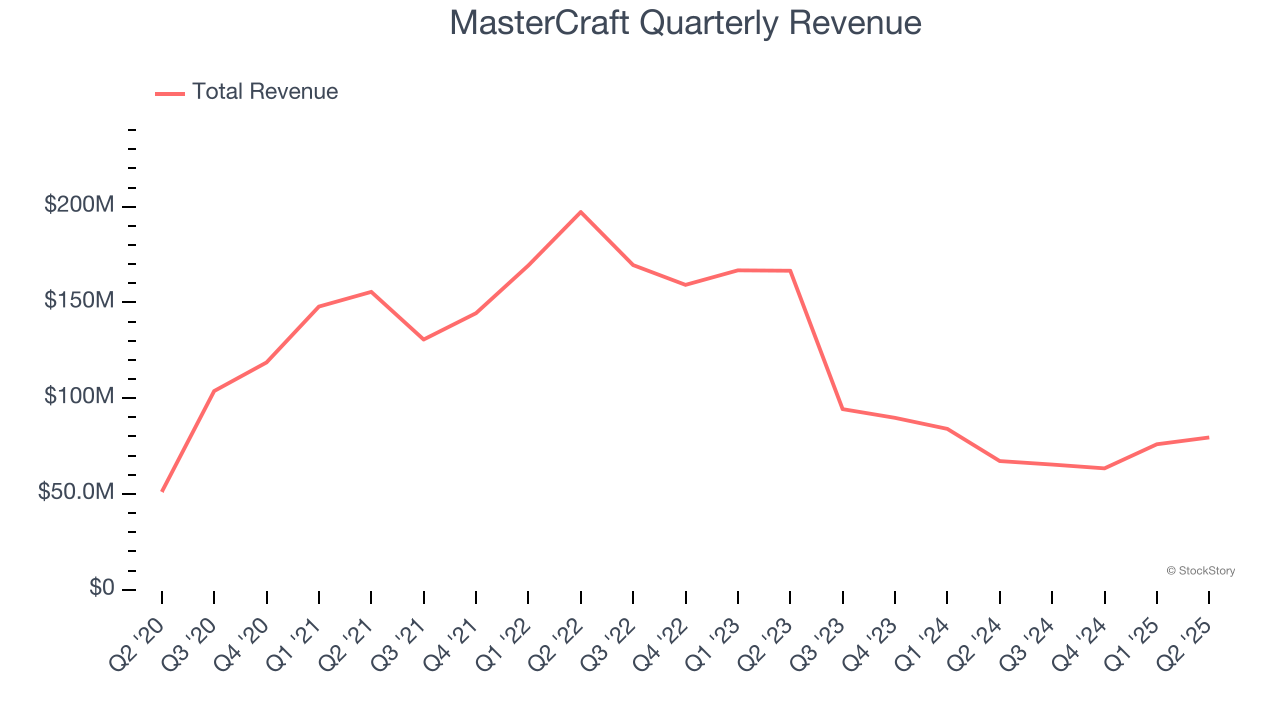

Sport boat manufacturer MasterCraft (NASDAQ: MCFT) beat Wall Street’s revenue expectations in Q2 CY2025, with sales up 18.4% year on year to $79.52 million. On the other hand, next quarter’s revenue guidance of $67 million was less impressive, coming in 13.7% below analysts’ estimates. Its non-GAAP profit of $0.40 per share was significantly above analysts’ consensus estimates.

Is now the time to buy MasterCraft? Find out by accessing our full research report, it’s free.

MasterCraft (MCFT) Q2 CY2025 Highlights:

- Revenue: $79.52 million vs analyst estimates of $70.06 million (18.4% year-on-year growth, 13.5% beat)

- Adjusted EPS: $0.40 vs analyst estimates of $0.18 (significant beat)

- Adjusted EBITDA: $9.53 million vs analyst estimates of $5.13 million (12% margin, 85.9% beat)

- Revenue Guidance for Q3 CY2025 is $67 million at the midpoint, below analyst estimates of $77.65 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.28 at the midpoint, beating analyst estimates by 7.7%

- EBITDA guidance for the upcoming financial year 2026 is $31.5 million at the midpoint, below analyst estimates of $31.78 million

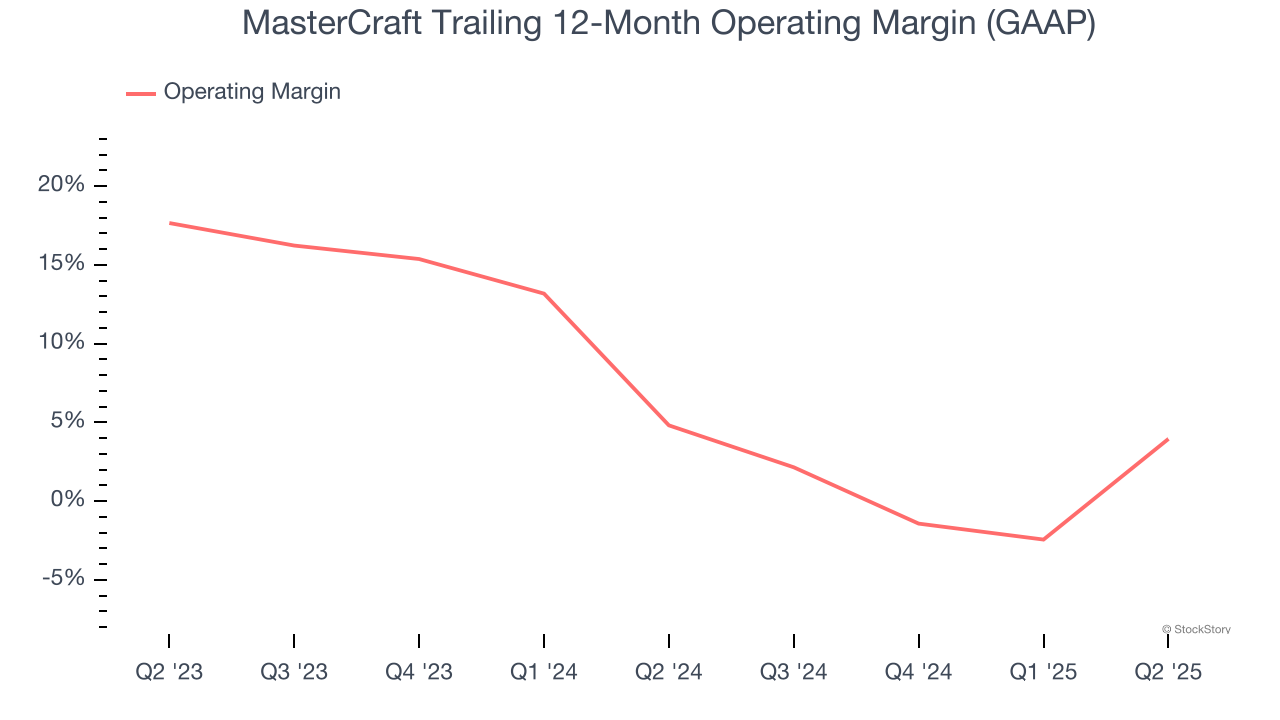

- Operating Margin: 7.5%, up from -17.8% in the same quarter last year

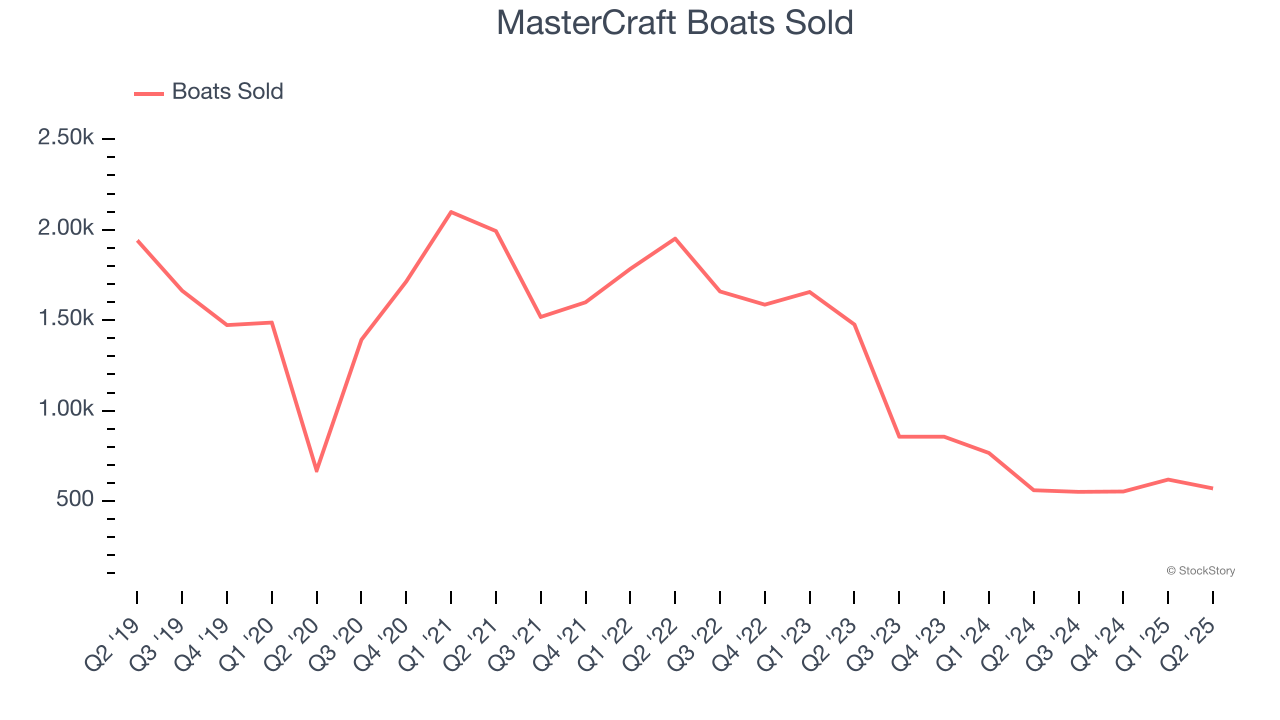

- Boats Sold: 570, up 10 year on year

- Market Capitalization: $347 million

Brad Nelson, Chief Executive Officer, commented, “MasterCraft executed well in fiscal 2025, successfully navigating a challenging economic and industry backdrop. In the face of low cycle volumes, we further strengthened dealer health, advanced our new product initiatives, and generated significant free cash flow. This enabled us to return nearly $10 million of capital to shareholders, underscoring our disciplined and value-enhancing approach to capital allocation.”

Company Overview

Started by a waterskiing instructor, MasterCraft (NASDAQ: MCFT) specializes in designing, manufacturing, and selling sport boats.

Revenue Growth

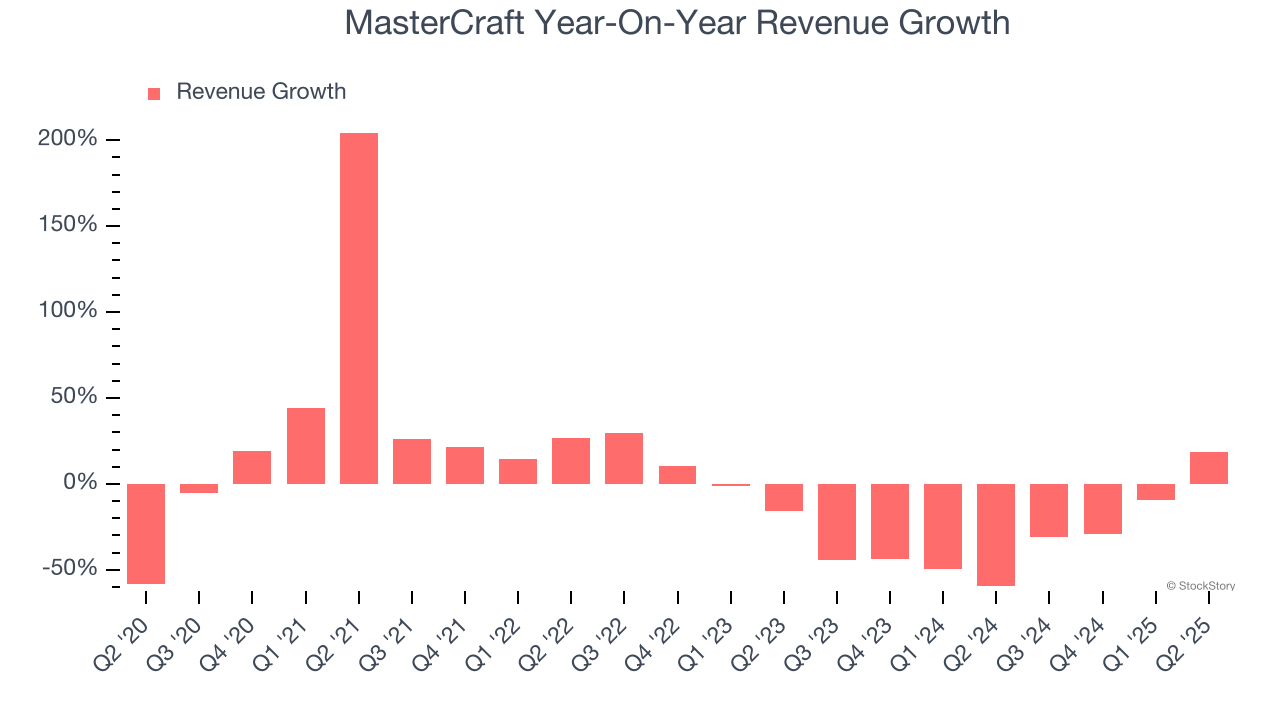

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, MasterCraft’s demand was weak and its revenue declined by 4.8% per year. This was below our standards and suggests it’s a lower quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. MasterCraft’s recent performance shows its demand remained suppressed as its revenue has declined by 34.5% annually over the last two years.

We can better understand the company’s revenue dynamics by analyzing its number of boats sold, which reached 570 in the latest quarter. Over the last two years, MasterCraft’s boats sold averaged 37.3% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, MasterCraft reported year-on-year revenue growth of 18.4%, and its $79.52 million of revenue exceeded Wall Street’s estimates by 13.5%. Company management is currently guiding for a 2.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.1% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and suggests its newer products and services will fuel better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

MasterCraft’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 4.4% over the last two years. This profitability was lousy for a consumer discretionary business and caused by its suboptimal cost structure.

This quarter, MasterCraft generated an operating margin profit margin of 7.5%, up 25.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

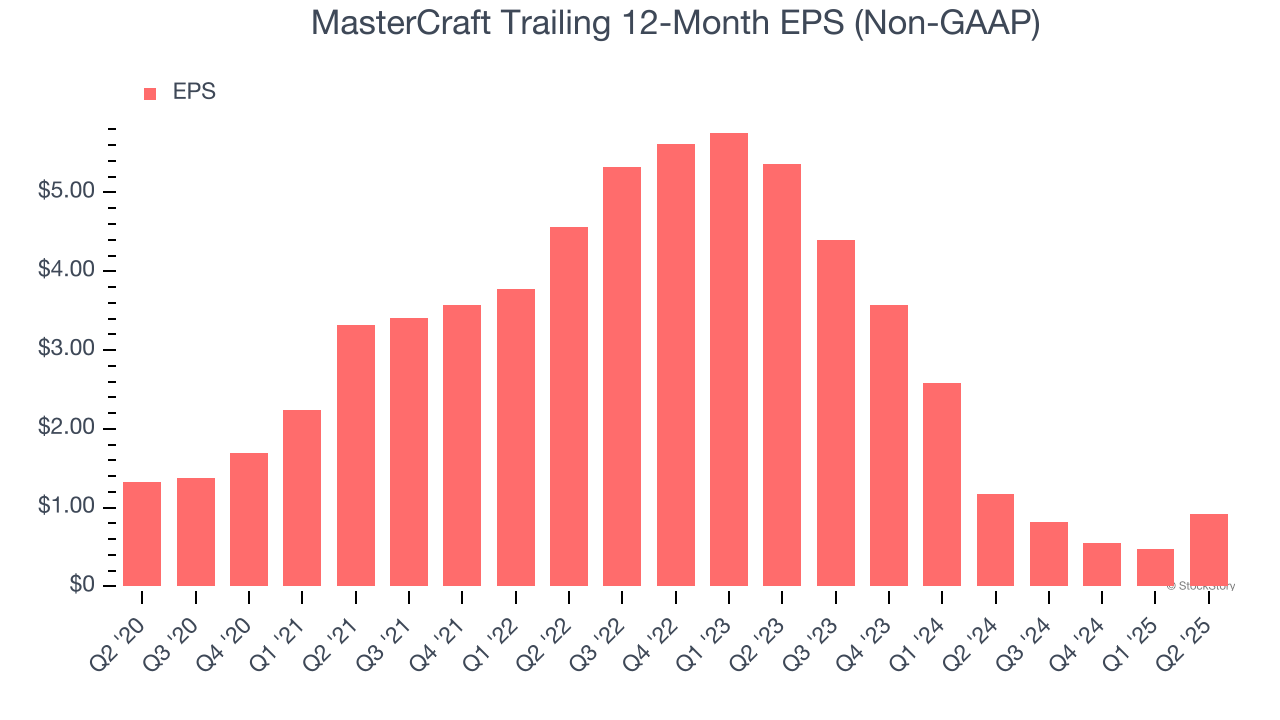

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for MasterCraft, its EPS declined by 7% annually over the last five years, more than its revenue. We can see the difference stemmed from higher taxes as the company actually improved its operating margin and repurchased its shares during this time.

In Q2, MasterCraft reported adjusted EPS of $0.40, up from negative $0.04 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects MasterCraft’s full-year EPS of $0.92 to grow 28.9%.

Key Takeaways from MasterCraft’s Q2 Results

It was good to see MasterCraft beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue guidance for the next quarter fell short of Wall Street’s estimates. Overall, this was still a decent quarter. The stock traded up 19.6% to $25 immediately after reporting.

So should you invest in MasterCraft right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.