Regional banking company FB Financial (NYSE: FBK) fell short of the market’s revenue expectations in Q2 CY2025, with sales falling 40.1% year on year to $76.86 million. Its non-GAAP profit of $0.88 per share was in line with analysts’ consensus estimates.

Is now the time to buy FB Financial? Find out by accessing our full research report, it’s free.

FB Financial (FBK) Q2 CY2025 Highlights:

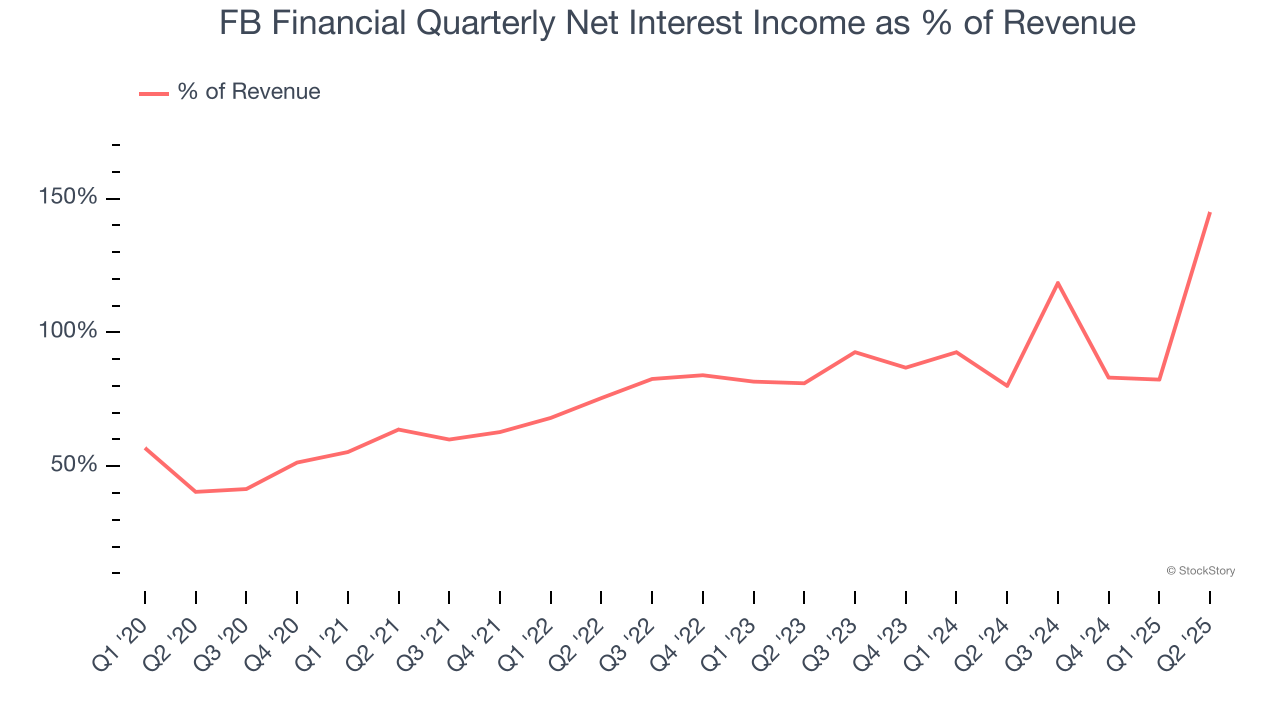

- Net Interest Income: $111.4 million vs analyst estimates of $111.3 million (8.6% year-on-year growth, in line)

- Net Interest Margin: 3.7% vs analyst estimates of 3.6% (11 basis point year-on-year increase, 11.3 bps beat)

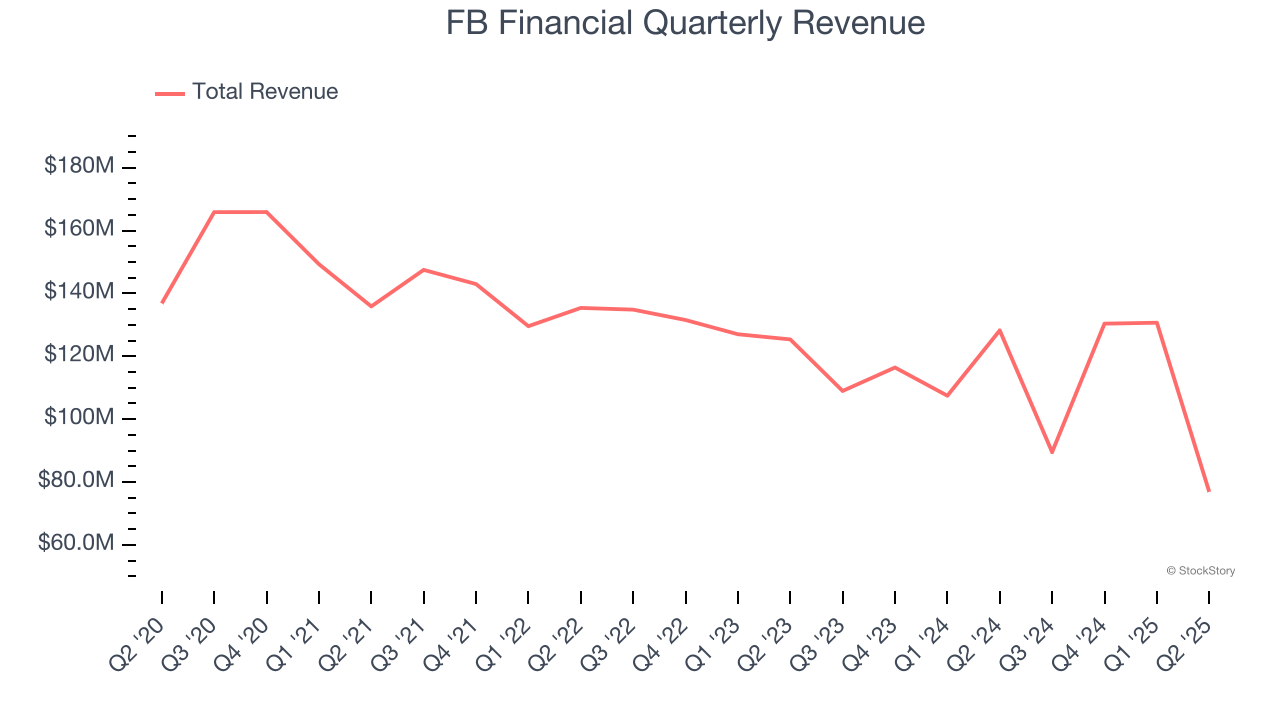

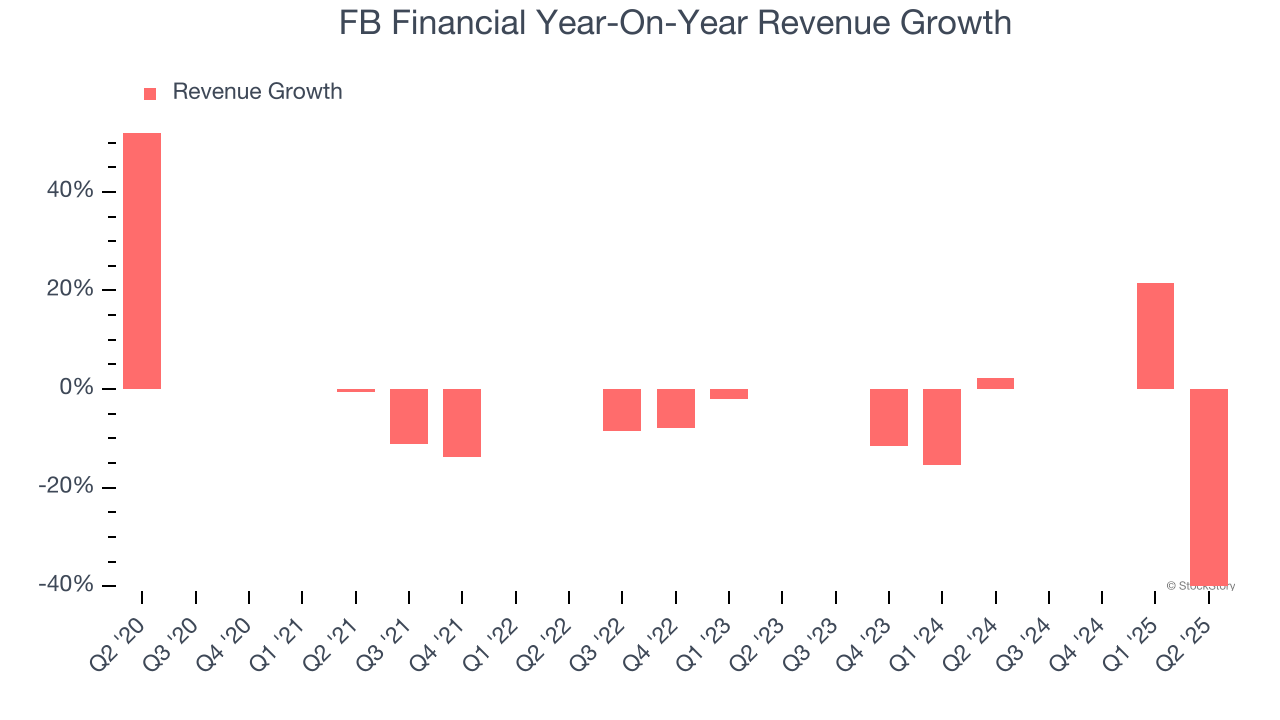

- Revenue: $76.86 million vs analyst estimates of $136 million (40.1% year-on-year decline, 43.5% miss)

- Efficiency Ratio: 56.9% vs analyst estimates of 57.9% (1 percentage point beat)

- Adjusted EPS: $0.88 vs analyst estimates of $0.88 (in line)

- Market Capitalization: $2.22 billion

President and Chief Executive Officer , Christopher T. Holmes stated, “The Company delivered solid operating results in the second quarter with growth in both loans and customer deposits, a healthy net interest margin and managed expense growth, along with strong capital and liquidity positions. Additionally, we repositioned our balance sheet by selling low-yielding securities which will further enhance both our liquidity and margin moving forward. With the momentum of the quarter, the impact of the balance sheet enhancements and the July 1st closing of the Southern States Bancshares, Inc. (“Southern States”) merger, we are well-positioned for the second half of the year.”

Company Overview

Founded in 1906 and operating through more than a century of economic cycles, FB Financial (NYSE: FBK) operates FirstBank, providing commercial and consumer banking services across Tennessee, Kentucky, Alabama, and North Georgia.

Sales Growth

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

Unfortunately, FB Financial struggled to consistently increase demand as its $427.4 million of revenue for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result, but there are still things to like about FB Financial.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. FB Financial’s recent performance shows its demand remained suppressed as its revenue has declined by 9.2% annually over the last two years.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, FB Financial missed Wall Street’s estimates and reported a rather uninspiring 40.1% year-on-year revenue decline, generating $76.86 million of revenue.

Net interest income made up 79.4% of the company’s total revenue during the last five years, meaning lending operations are FB Financial’s largest source of revenue.

Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

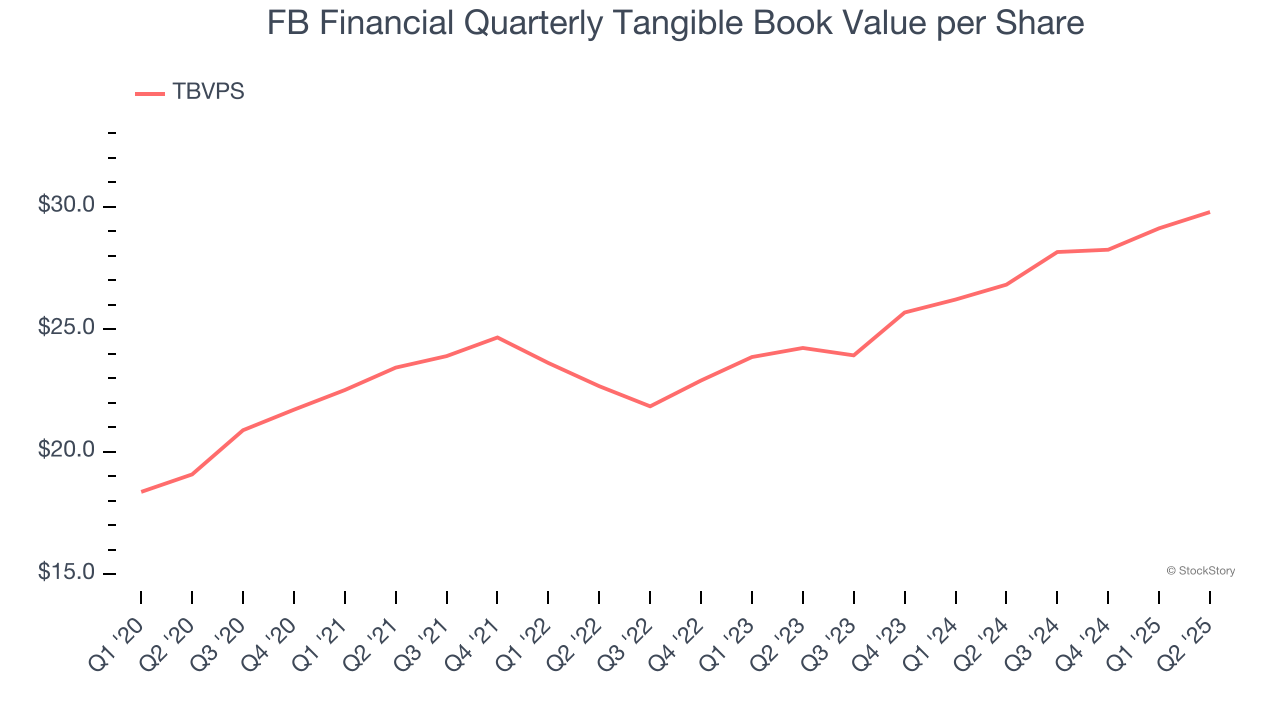

Tangible Book Value Per Share (TBVPS)

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. EPS can become murky due to acquisition impacts or accounting flexibility around loan provisions, and TBVPS resists financial engineering manipulation.

FB Financial’s TBVPS grew at an exceptional 9.3% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 10.9% annually over the last two years from $24.23 to $29.78 per share.

Over the next 12 months, Consensus estimates call for FB Financial’s TBVPS to grow by 9.5% to $32.60, decent growth rate.

Key Takeaways from FB Financial’s Q2 Results

We struggled to find many positives in these results as its revenue missed significantly due to a sizeable realized loss on the sale of some low-yielding debt securities. Overall, this was a weaker quarter. The stock traded down 7.6% to $45.44 immediately after reporting.

FB Financial may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.