Valued at $12.8 billion by market cap, DaVita Inc. (DVA) is a prominent healthcare company specializing in kidney care and dialysis services for patients with chronic kidney disease and end-stage renal disease. Headquartered in Denver, the company operates one of the world’s largest dialysis networks, providing treatment through thousands of outpatient centers as well as home dialysis programs across the U.S. and international markets.

Shares of this kidney care giant have exceeded the broader market over the past year. DVA has soared 38.9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 26.6%. In 2026, DVA stock is up 76.5%, compared to the SPX’s 8.1% rise on a YTD basis.

Narrowing the focus, DVA has also outpaced the SPDR S&P Health Care Services ETF (XHS), which has soared 14.8% over the past year. Moreover, the ETF’s 6.3% gain on a YTD basis trails the stock’s double-digit returns over the same time frame.

On May 5, DaVita released its FY2026 first-quarter earnings, and its shares popped 23.5% in the next trading session. Revenue rose 6% year over year to $3.42 billion, while adjusted EPS jumped roughly 43.5% annually to $2.87, comfortably ahead of analyst estimates, thanks to improving dialysis treatment volumes and better cost control.

For the current fiscal year, ending in December, analysts expect DVA’s EPS to grow 39.8% to $15.07 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

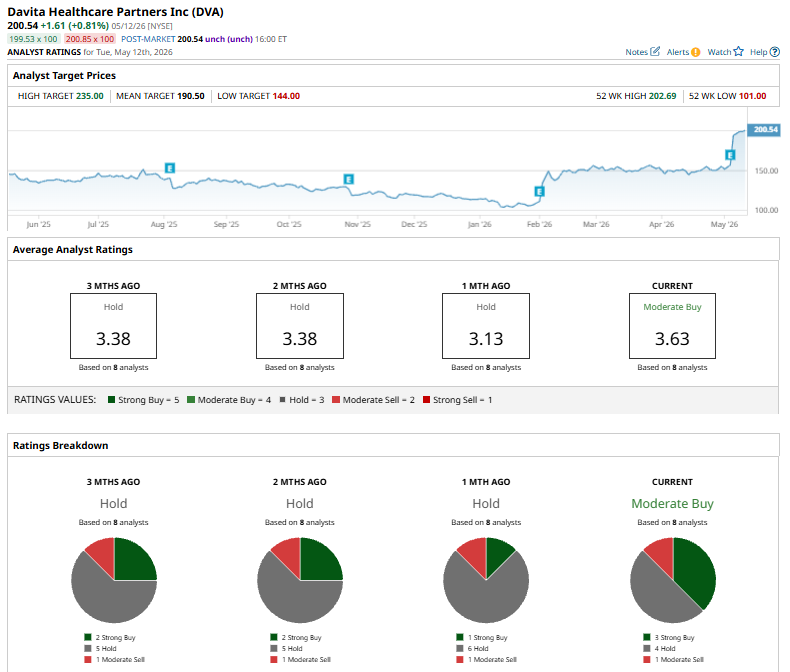

Among the eight analysts covering DVA stock, the consensus is a “Moderate Buy.” That’s based on three “Strong Buy” ratings, four “Holds,” and one “Moderate Sell.”

The consensus is bullish than a month ago when the stock had an overall “Hold” rating.

On May 11, analysts at TD Cowen raised their price target on DaVita to $201 from $144 while maintaining a “Hold” rating on the stock. The firm updated its outlook after DaVita delivered stronger-than-expected Q1 results, driven by better performance in non-acquired dialysis treatments and improved operational trends.

The stock currently trades above its mean price target of $190.50, and the Street-high price target of $235 suggests an ambitious upside potential of 17.2%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Rocket Lab Stock Is Getting a Major Lift. Investors Are Betting on Its Neutron Launch Later This Year.

- Under Armour Stock Plummets as Sales Continue to Decline

- Zebra Technologies Surges Following Q1 Earnings. What Comes Next for ZEBRA Stock.

- SNDK Stock Alert: SanDisk Falls Amid Broader Chip Pullback