Datadog, Inc. (DDOG), headquartered in New York, operates an observability and security platform for cloud applications. Valued at $70.5 billion by market cap, the company offers cloud-based monitoring and analytics platform which integrates and automates infrastructure monitoring, application performance monitoring, and log management for real-time observability of customers.

Shares of this cloud monitoring giant have outperformed the broader market considerably over the past year. DDOG has gained 76.3% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 26.6%. In 2026, DDOG stock is up 47%, surpassing the SPX’s 8.1% rise on a YTD basis.

Zooming in further, DDOG has also outpaced the SPDR S&P Software & Services ETF (XSW). The exchange-traded fund has declined about 13.3% over the past year. Moreover, DDOG returns on a YTD basis outshines the ETF’s 16.6% losses over the same time frame.

DDOG’s growth is fueled by strong demand from both AI-native firms and traditional enterprises. Big wins with AI research and hyperscale customers using Datadog’s GPU monitoring for AI workloads, plus broader adoption as 56% of clients now use 4+ products, drove the upside. Moreover, new launches like MCP Server for live debugging, AI security agents, and GPU monitoring, plus FedRAMP High certification and a planned UK data center, position it for regulated markets. Furthermore, management raised guidance citing broad-based ARR growth, AI-driven demand, and deeper product adoption, though continued growth hinges on R&D investment and meeting evolving data residency/security needs.

On May 7, DDOG shares surged 31.3% after reporting its Q1 results. Its adjusted EPS of $0.60 topped Wall Street expectations of $0.50. The company’s revenue was $1 billion, topping Wall Street forecasts of $956.9 million. DDOG expects full-year adjusted EPS in the range of $2.36 to $2.44, and revenue ranging from $4.30 billion to $4.34 billion.

For the current fiscal year, ending in December, analysts expect DDOG’s EPS to decline 21.4% to $0.33 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

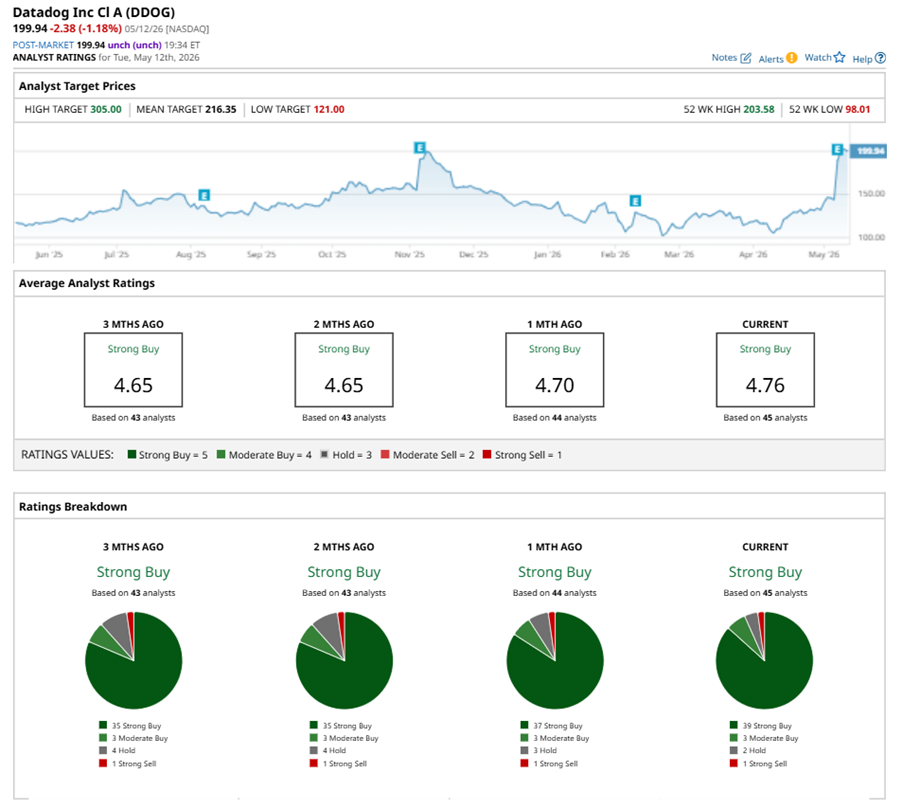

Among the 45 analysts covering DDOG stock, the consensus is a “Strong Buy.” That’s based on 39 “Strong Buy” ratings, three “Moderate Buys,” two “Holds,” and one “Strong Sell.”

This configuration is more bullish than a month ago, with 37 analysts suggesting a “Strong Buy.”

On May 8, Wedbush kept an “Outperform” rating on DDOG and raised the price target to $220, implying a potential upside of 10% from current levels.

The mean price target of $216.35 represents an 8.2% premium to DDOG’s current price levels. The Street-high price target of $305 suggests an ambitious upside potential of 52.5%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart