Beyond the obvious names, some of the enticing opportunities in artificial intelligence (AI) are hidden deep in the semiconductor supply chain. One such under-the-radar player is STMicroelectronics (STM), which recently reported a stunning 86% increase in profits in Q1, fueled by its growing role in AI infrastructure, data centers, and next-generation electronics. And that’s not all. Analysts project triple-digit earnings growth for 2026.

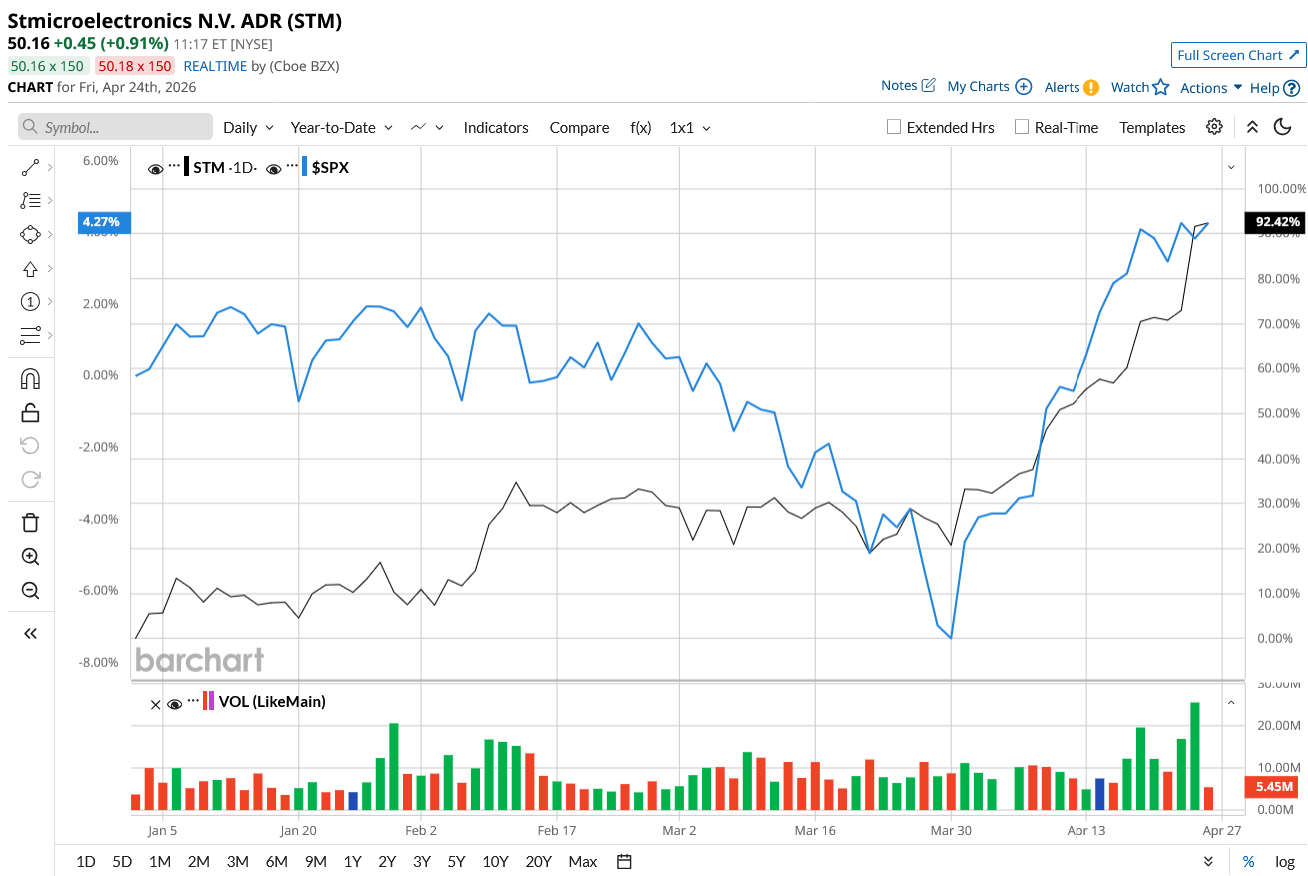

STM stock has surged a whopping 93% year-to-date (YTD), outperforming all the big tech names in the Magnificent Seven, as well as the broader market. The stock has also surged 115% over the past 52 weeks.

Should you grab STM stock now?

A Quiet Semiconductor Leader Steps Into the Spotlight

STMicroelectronics has long operated outside the spotlight, but its recent Q1 report is forcing investors to pay attention. Valued at $44.4 billion, STMicroelectronics is a global semiconductor manufacturer that designs and manufactures chips used in a wide range of electronic systems, from smartphones and cars to industrial machines and AI data centers.

The company reported $3.10 billion in revenue, an increase of 23% year-over-year (YoY). Revenue also included $40 million from the recently acquired NXP MEMS sensor business. STM completed the acquisition in February, which is intended to improve both product capabilities and long-term growth prospects. MEMS sensors play an important role in enabling intelligent systems ranging from smartphones and wearables to industrial automation and robots. Following the integration, this acquisition will boost STM's position in sensing technology.

All of its segments, including the Analog Products, MEMS and Sensors, Embedded Processing, and Optical Communications, experienced double-digit growth, offsetting the 1.8% dip in Power and Discrete products.

The real star of the first-quarter report was the explosive earnings growth. Adjusted earnings per share increased 85.7% to $0.13 per share, signaling improved margins, a robust product mix, and rising exposure to high-growth AI-driven sectors. Despite the strong earnings growth, the company's free cash flow came in negative at $723 million, largely due to an $895 million cash outflow tied to the MEMS acquisition. The company is actively reshaping its manufacturing footprint, optimizing costs, and investing in future growth opportunities. These expenses could put short-term pressures but also could improve profitability over time.

Strategic Partnerships Fueling the Next Growth Wave

Looking ahead to the second quarter, management expects a 25% jump in revenue to roughly $3.45 billion at the midpoint. For the full year, the company expects double-digit revenue growth, driven by both existing customer programs and new AI-related opportunities.

STM has also strengthened its strategic partnership with Amazon's (AMZN) AWS through a multi-year, multibillion-dollar commercial agreement centered on high-performance compute infrastructure. Additionally, it has collaborated with Nvidia (NVDA) to integrate sensors, microcontrollers, and motor control solutions into robotics and AI ecosystems, with the goal of improving efficiency and scalability. This expanding network of strategic partnerships is expected to boost its data center revenue. Management anticipates that data center revenue will exceed $500 million in 2026 and well over $1 billion in 2027.

Management’s guidance implies that the earnings surge in the quarter was not a one-off case but part of a larger structural shift. In fact, analysts expect a dramatic increase in earnings over the next two years. In 2026, EPS is expected to increase by 124% to 1.19, followed by another 75% to $2.08 per share.

Why This “Hidden” AI Stock May Not Stay Hidden

STMicroelectronics isn’t a flashy AI company building chatbots or training models. Instead, it works behind the scenes, supplying critical technology that enables AI systems to function properly. This makes the company indispensable in the rapidly evolving AI market.

Currently, STM stock is valued at 22x forward 2027 earnings, making it a reasonable buy. The company operates in a less visible layer of the manufacturing chain. However, STM may not stay hidden for long. Its combination of strong earnings growth, expanding AI exposure, strategic partnerships, and diversified revenue streams makes it a compelling growth story in today’s market. Investors are starting to recognize STM’s value, which could eventually make the stock expensive.

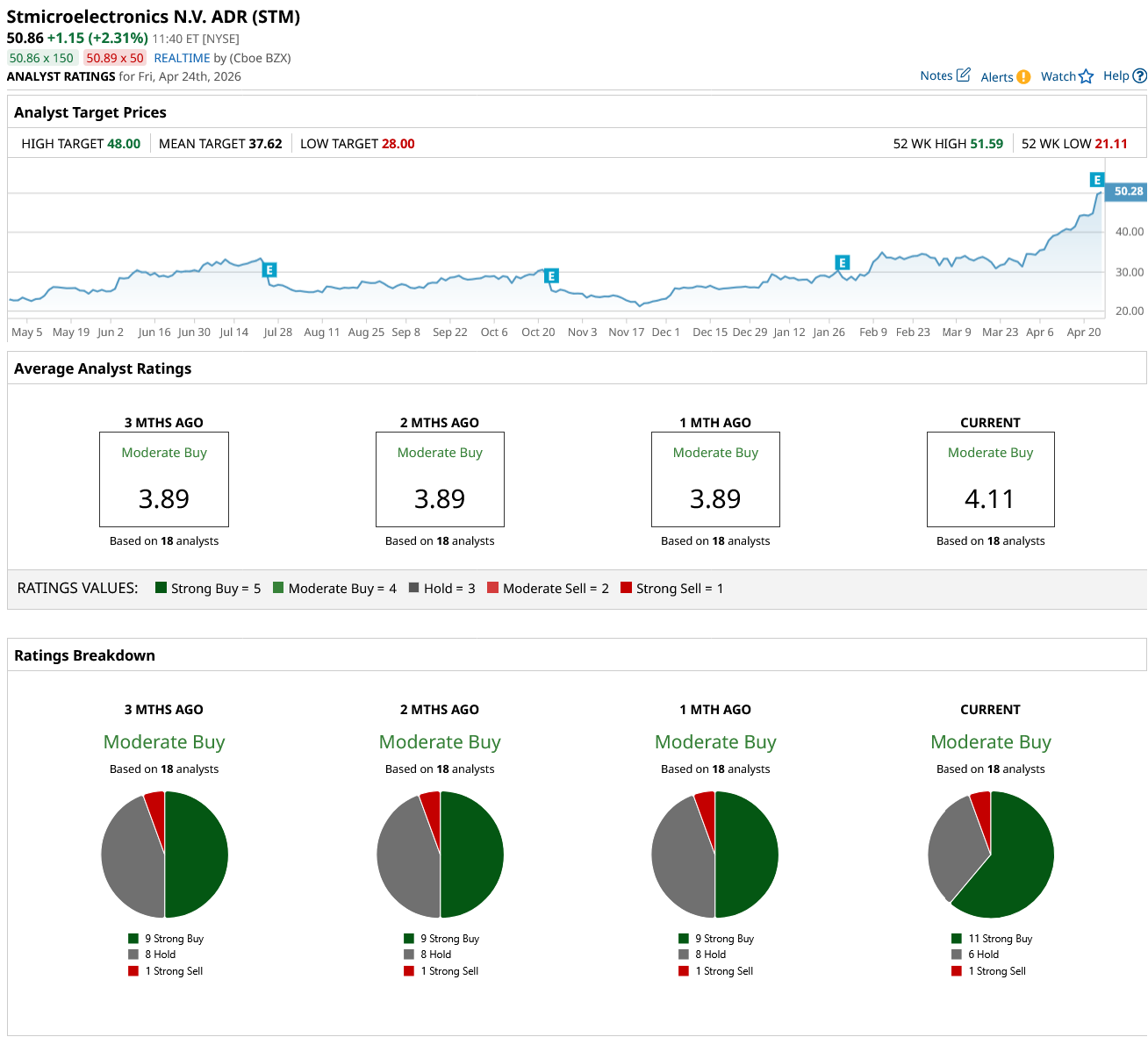

Overall, Wall Street believes STM stock is a consensus “Moderate Buy.” Out of the 18 analysts who cover the stock, 11 rate it a “Strong Buy,” six rate it a “Hold,” and one says it is a “Strong Sell.” Given its dramatic rally this year, the stock has surpassed both its average target price and high price estimate.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart