The troubles for AI infrastructure company Super Micro Computer (SMCI) seem to show no signs of abating. After accounting issues led to its delisting and auditors handing in their resignations, the company found itself in murky waters again when it was accused of smuggling Nvidia (NVDA) chips to China. While a co-founder and a contractor face prosecution, there has been some dire but not unexpected fallout.

Cloud giant Oracle (ORCL) has supposedly suspended a contract with the company, which entailed Super Micro delivering Nvidia's GB300 NVL72 racks to the company. At an estimated price of $3.5 million per rack, the revenue hit is expected to be around $1.1 and $1.4 billion. For context, Super Micro's net sales for the latest quarter were at $12.7 billion, which implies a blow of 10%.

And if all this was not enough, the company has been saddled with supply chain issues as well.

About Super Micro Computer

Founded in 1993, Super Micro is a high-performance server and data center infrastructure provider. Its core offerings include AI servers, data center infrastructure, storage, cloud systems, and edge/5G infrastructure. Its customers span the entire spectrum of the AI ecosystem, including hyperscalers, enterprises, cloud providers, and AI startups.

Valued at a market cap of $17.5 billion, SMCI stock is down 3% on a year-to-date (YTD) basis.

So, is SMCI worth taking a shot at now, or is it too fraught with risks? Let's find out.

Issues Persist

Before delving deeper, I must concede that since my last analysis on Super Micro, shares of the company are up 30%. This is definitely impressive when one considers that it happened in about a fortnight. However, the issues highlighted continue to plague the company, and new ones (read: Oracle) continue to crop up. In fact, in my last analysis, I had pointed out how these reputational and regulatory issues would drive hyperscalers away from the company, and it looks like that is precisely what happened in the case of Oracle.

Moreover, the business was already caught in a difficult position well before things came to a head, struggling to protect its margins even as revenues expanded and finding it increasingly difficult to secure the outside capital needed to fund that growth, a situation made considerably worse by the governance concerns that had been hanging over the company for some time.

Also, its relationship with its most vital partner, Nvidia (NVDA), will also be in jeopardy if the company doesn't firefight its governance issues ASAP. Super Micro's dependence on Nvidia has only deepened in recent years, with it being estimated that from 31% in fiscal 2023, the company's sourcing of components from Nvidia has surged to about 64.4% in fiscal 2025. For a market leader like Nvidia, associating with a company with so many governance hazards will not do it any good, especially amid intense competition from the likes of AMD (AMD) and Broadcom (AVGO).

Strong Q2 (But Does That Even Count?)

Super Micro Computer delivered an impressive fiscal Q2 2026 performance, delivering a rare double beat by surpassing analyst expectations on both revenue and earnings. The company posted net sales of $12.7 billion, more than twice the $5.7 billion recorded in the same quarter a year earlier. Meanwhile, earnings per share climbed 17% from the prior year period to $0.69, clearing the Wall Street consensus estimate of $0.49 by a meaningful margin.

Looking ahead, management issued Q3 2026 guidance calling for net sales of no less than $12.3 billion alongside earnings per share of at least $0.60. Those figures point to year-over-year (YoY) revenue growth of roughly 167% and earnings expansion of approximately 94%, underscoring the momentum the business continues to build.

The cash flow picture told a more complicated story, though. Through the first six months of the fiscal year, the company recorded an operating cash outflow of $941.4 million, a notable reversal from the $169.1 million in positive operating cash flow generated during the comparable stretch a year ago. That said, the balance sheet remained on solid footing, with cash and equivalents of roughly $4.19 billion at quarter's end, a figure that comfortably exceeded its near-term debt obligations.

From a valuation standpoint, the stock looks reasonably priced relative to the broader sector. Shares currently trade at 12.96 times forward earnings and just 0.42 times forward sales, both of which sit well beneath the relevant sector medians.

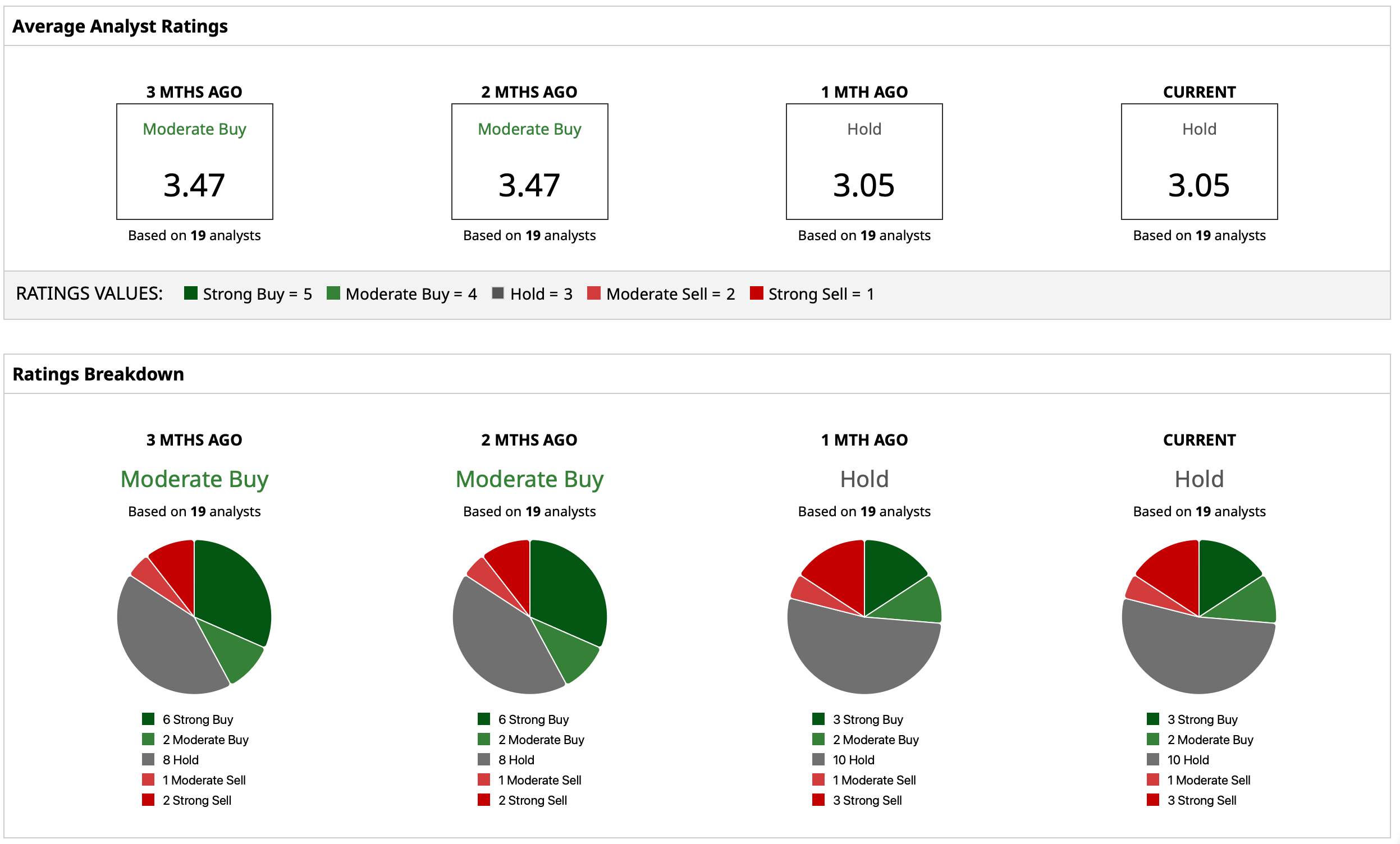

Analyst Opinion on SMCI Stock

Considering this, analysts have an overall rating of a “Hold” rating on SMCI stock. The mean price target of $33.33 implies potential upside of about 24.6% from current levels. Out of 19 analysts covering SMCI stock, three have a “Strong Buy” rating, two have a “Moderate Buy” rating, 10 have a “Hold” rating, one has a “Moderate Sell” rating, and three have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart