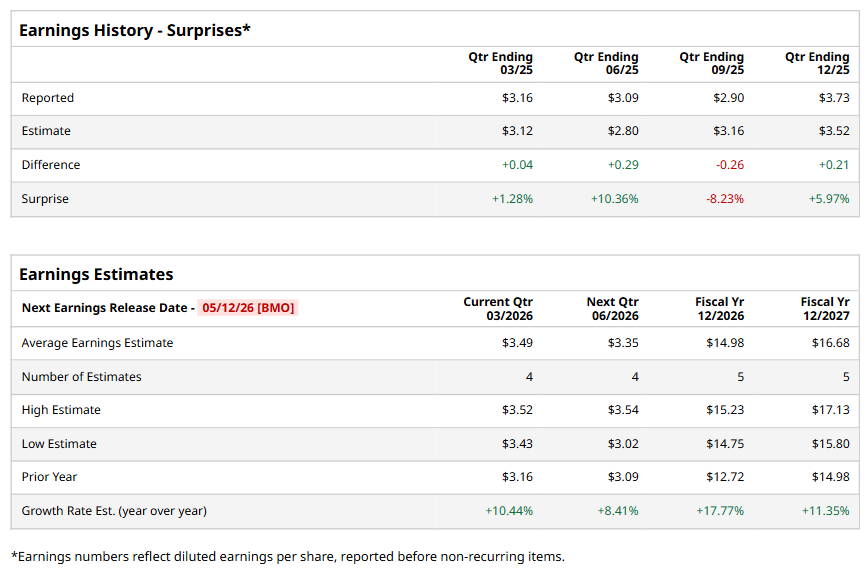

Lincolnshire, Illinois-based Zebra Technologies Corporation (ZBRA) provides enterprise asset intelligence solutions in the automatic identification and data capture solutions industry. Valued at $11.6 billion by market cap, the company offers mobile computers, printers, barcode scanners, RFID, locating systems hardware, software, interactive kiosks, printing supplies, and accessories. The leading digital solutions provider is expected to announce its fiscal first-quarter earnings for 2026 before the market opens on Tuesday, May 12.

Ahead of the event, analysts expect ZBRA to report a profit of $3.49 per share on a diluted basis, up 10.4% from $3.16 per share in the year-ago quarter. The company beat the consensus estimates in three of the last four quarters while missing the forecast on another occasion.

For the full year, analysts expect ZBRA to report EPS of $14.98, up 17.8% from $12.72 in fiscal 2025. Its EPS is expected to rise 11.4% year over year to $16.68 in fiscal 2027.

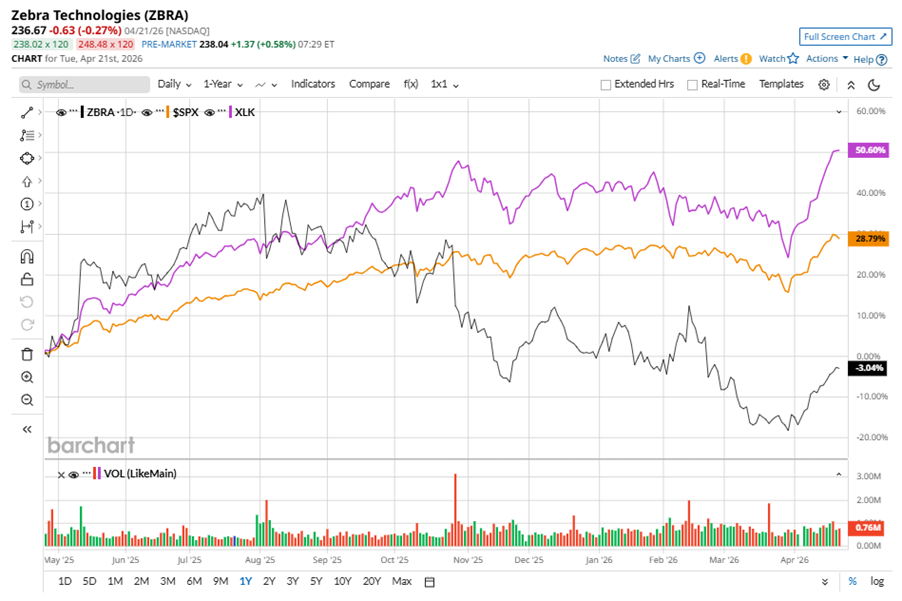

ZBRA stock has underperformed the S&P 500 Index’s ($SPX) 33.6% gains over the past 52 weeks, with shares up 6.6% during this period. Similarly, it notably underperformed the State Street Technology Select Sector SPDR ETF’s (XLK) 64.7% gains over the same time frame.

ZBRA underperformed as new U.S. tariffs sparked trade uncertainty, raising supply chain and cost risks tied to its global manufacturing footprint.

On Feb. 12, ZBRA shares closed up by 8.6% after reporting its Q4 results. Its adjusted EPS of $4.33 did not meet Wall Street expectations of $4.34. The company’s revenue was $1.48 billion, beating Wall Street forecasts of $1.46 billion. The company expects full-year adjusted EPS in the range of $17.70 to $18.30.

Analysts’ consensus opinion on ZBRA stock is reasonably bullish, with an overall “Moderate Buy” rating. Out of 17 analysts covering the stock, 11 advise a “Strong Buy” rating, one suggests a “Moderate Buy,” and five give a “Hold.” ZBRA’s average analyst price target is $336, indicating an ambitious potential upside of 42% from the current levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Dear MaxLinear Stock Fans, Mark Your Calendars for April 23

- SanDisk: Is a 20x Surge Just the Beginning or a Peak for This AI Pure-Play?

- Mizuho Analysts Are Bullish on Custom Chips: Broadcom Could Have 87% Compound Annual Growth Rate Through 2028

- Catching the Falling Knife: Are These 4 Loser Stocks Down 50% or More Worth the Risk?