Semiconductor stocks have been some of the market’s biggest winners over the past few years. As artificial intelligence (AI), electric vehicles (EVs), and advanced computing keep driving chip demand, investors continue to look for the companies building the tools behind the boom. That has put chip equipment makers like Applied Materials (AMAT) in the spotlight.

Now, AMAT has an even more interesting angle. According to a recent report, Tesla (TSLA) CEO Elon Musk’s Terafab project has reached out to Applied Materials — along with Lam Research (LRCX) and Tokyo Electron (TOELY) — as Tesla, SpaceX, and xAI work to build out a domestic chipmaking push. That does not mean AMAT stock is suddenly a guaranteed winner, but it does show that one of the most important names in semiconductor equipment could play a bigger role in one of the most ambitious manufacturing projects in the market.

For investors, the key question is simple: does this new connection to Terafab make AMAT stock a buy?

Applied Materials Rides the AI Rally

Applied Materials is a top supplier of the machines used to build semiconductors, flat panels and solar cells. In other words, it sells the high-tech equipment that layers, etches and inspects silicon wafers. That means AMAT stock rides the waves in chip demand, like the current one for AI and memory chips. The firm has unveiled new tools, too, most notably deposition and etch systems for the “angstrom-era” 2-nanometer (2nm) and beyond chips. Plus, in R&D, Applied Materials recently launched an “EPIC Center” for advanced chip research; Samsung will join as a partner at the new center.

On March 22, Applied Materials earned a spot in the S&P 100, which shows its large size and market status. Moreover, the company recently raised its quarterly dividend 15% from $0.46 to $0.53, a sign of confidence in cash flow.

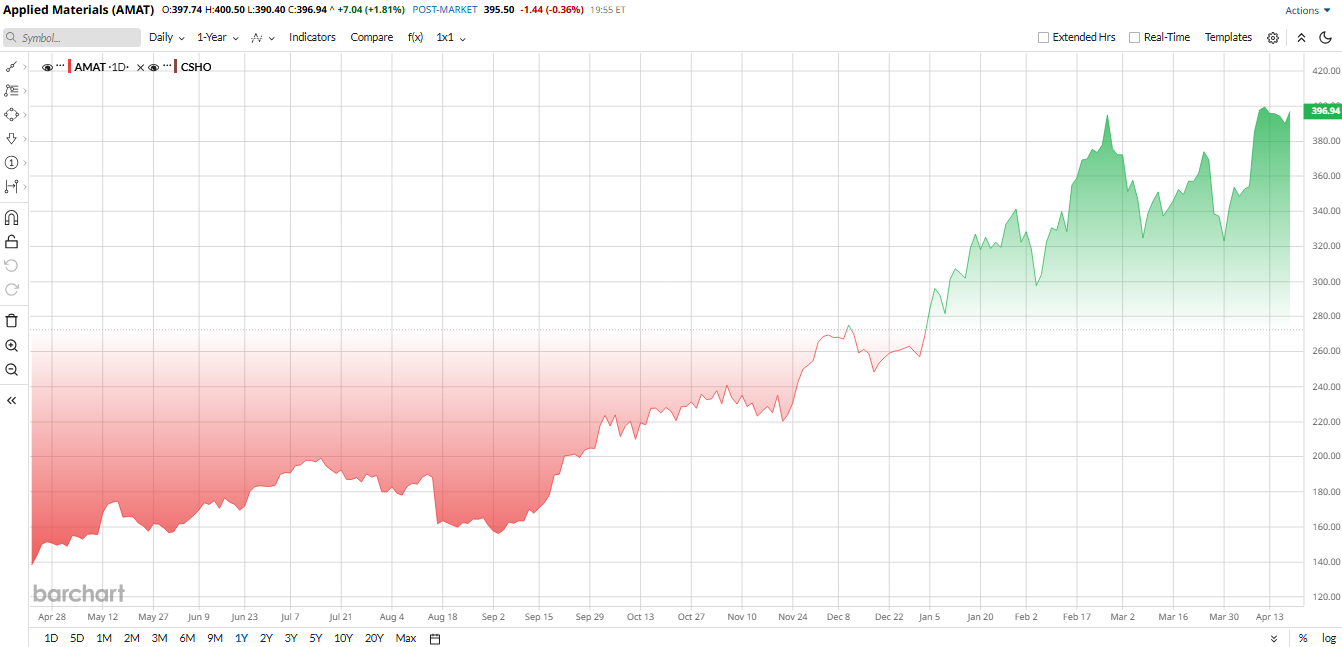

AMAT stock has climbed sharply of late. Shares are up about 54% year-to-date (YTD) and have climbed 186% in the past 12 months. The rally has been fueled by surging demand for AI chips and improving semiconductor spending. Technically, the stock trades well above its moving averages, changing hands around $396 versus its 50-day average at $363 and 200-day average at $262. In short, AMAT stock is well into a bullish trend as of April 2026.

Even after the run-up, AMAT trades at rich multiples. Its forward price-to-earnings (P/E) ratio is around 35 times, far above the tech sector median of 21 times. The price-to-sales (P/S) multiple is also about 10.9 times versus roughly 4.1 times for the semiconductor equipment industry. So, it's clear that the stock looks expensive on these metrics relative to peers. But this also reflects high growth expectations and a long-term uptrend, which means shares aren’t “cheap” by historical norms.

Tesla Terafab News and Impact

Reports recently confirmed that Elon Musk's Terafab chip project has been asking Applied Materials for quotes on equipment. That news briefly lifted AMAT stock as investors cheered the prospect of a huge new customer.

The logic: if Tesla really builds its own AI chip plant targeting 2029 production, it could need tons of wafer fab tools, wafer deposition, etch, cleaning and more — all things that Applied Materials sells.

Of course, Terafab is still in its early stages. Musk’s team is in fact-finding mode, so there’s no confirmed order for Applied Materials yet. Traders seem to agree it’s potentially good news, but not a guaranteed sales boost in the near term.

For now, investors are watching to see how deep Applied Materials' footprint becomes. But at a minimum, the Terafab talk highlights the company’s key role in next-gen chipmaking.

Applied Materials Beats Q1 Earnings

Applied Materials reported first-quarter results in mid-February, with revenue slipping slightly but profits and cash flow improving. The company posted revenue of $7.01 billion, down about 2% from a year earlier. CEO Gary Dickerson said demand tied to AI is driving investment in chipmaking equipment and expects the company’s semiconductor business to grow more than 20% this year.

Net income rose sharply to $2.03 billion, up 71% from a year earlier, while adjusted EPS came in at $2.38, roughly flat year-over-year (YOY) but slightly ahead of expectations.

Cash generation remained strong. Non-GAAP free cash flow reached about $1.04 billion, up 91% from the prior year. The company ended the quarter with around $7.2 billion in cash. CFO Brice Hill said Applied Materials has expanded its manufacturing capacity and increased inventory to manage potential supply disruptions.

For the current quarter, Applied expects revenue of about $7.65 billion, plus or minus $500 million, and adjusted EPS of about $2.64, with a margin of $0.20 on either side. Analysts on average expect earnings of $2.66 per share for the quarter and about $11.10 for fiscal 2026, implying mid-teens growth YOY.

What Are Analysts Saying About Applied Materials Stock?

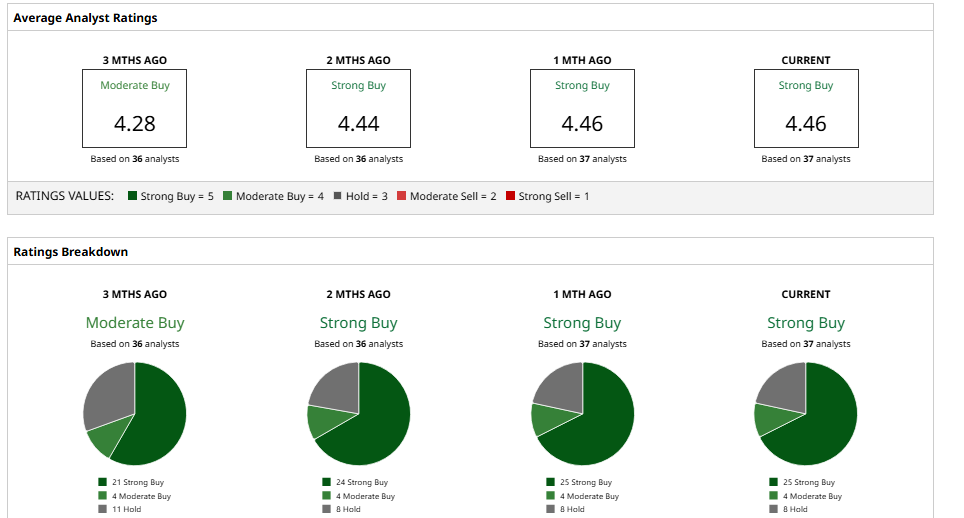

Wall Street seems to be largely bullish on Applied Materials' future prospects. Several analysts have raised targets again following the strong quarter. For example, Morgan Stanley analyst Shane Brett reiterated an “Overweight” rating on the stock and bumped his 12-month target to $432.

Likewise, Deutsche Bank analyst Melissa Weathers upgraded AMAT stock to “Buy” from “Hold” with a $390 target, arguing that wafer fab equipment (WFE) spending is improving and that AMAT could outperform current forecasts. Susquehanna’s Mehdi Hosseini also recently boosted his target to $500, citing new 2nm chip tool launches as a catalyst.

Overall, the consensus rating among 37 analysts is a “Strong Buy.” The average price target is $409.59, which suggests 3% potential upside from current levels. That modest implied upside means that most big firms already expect continued growth. While AMAT stock’s run has been so strong that shares may now trade ahead of the fundamentals, analysts are overall positive on the name.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Should You Buy the Dip in United Airlines Stock?

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?

- AMD Stock Just Hit New All-Time Highs. Should You Buy Shares Here?