The past six months have been a windfall for Viasat’s shareholders. The company’s stock price has jumped 80.2%, hitting $62.46 per share. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Viasat, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Viasat Not Exciting?

Despite the momentum, we’re cautious about Viasat. Here are three reasons why there are better opportunities than VSAT, plus one stock we’d rather own.

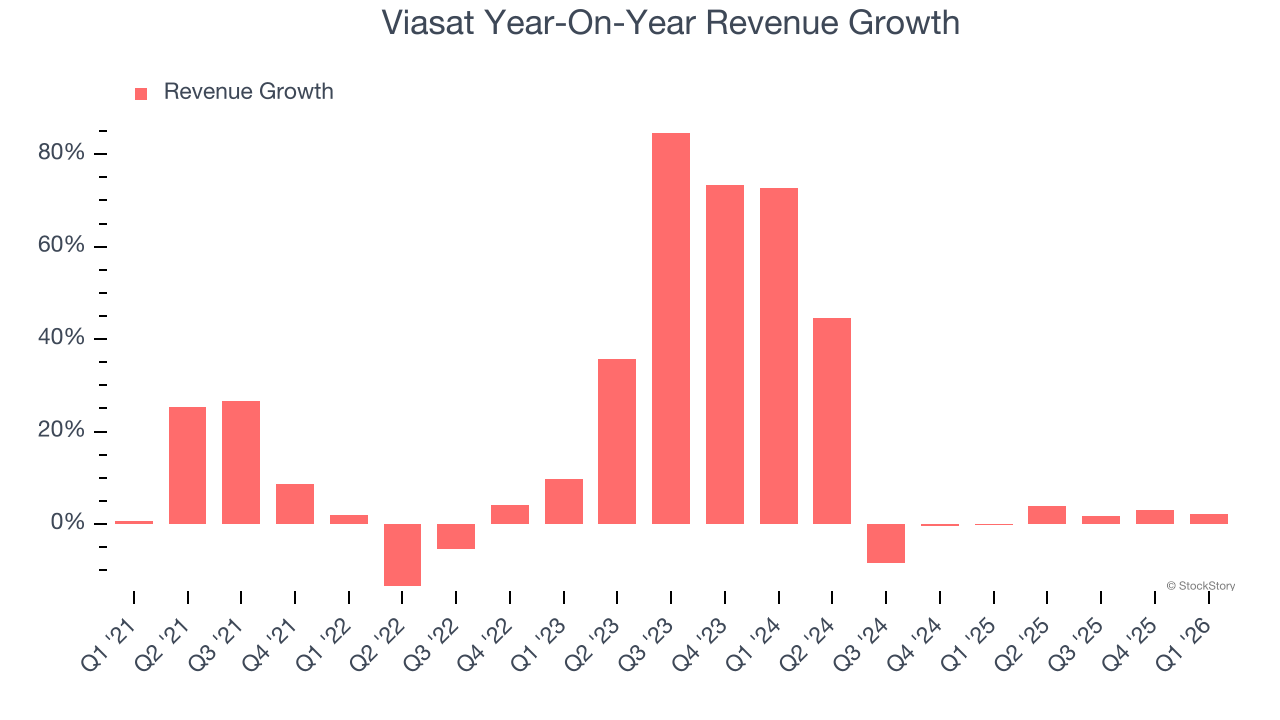

1. Lackluster Revenue Growth

Long-term growth is the most important, but within business services, a stretched historical view may miss new innovations or demand cycles. Viasat’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.1% over the last two years was well below its five-year trend.

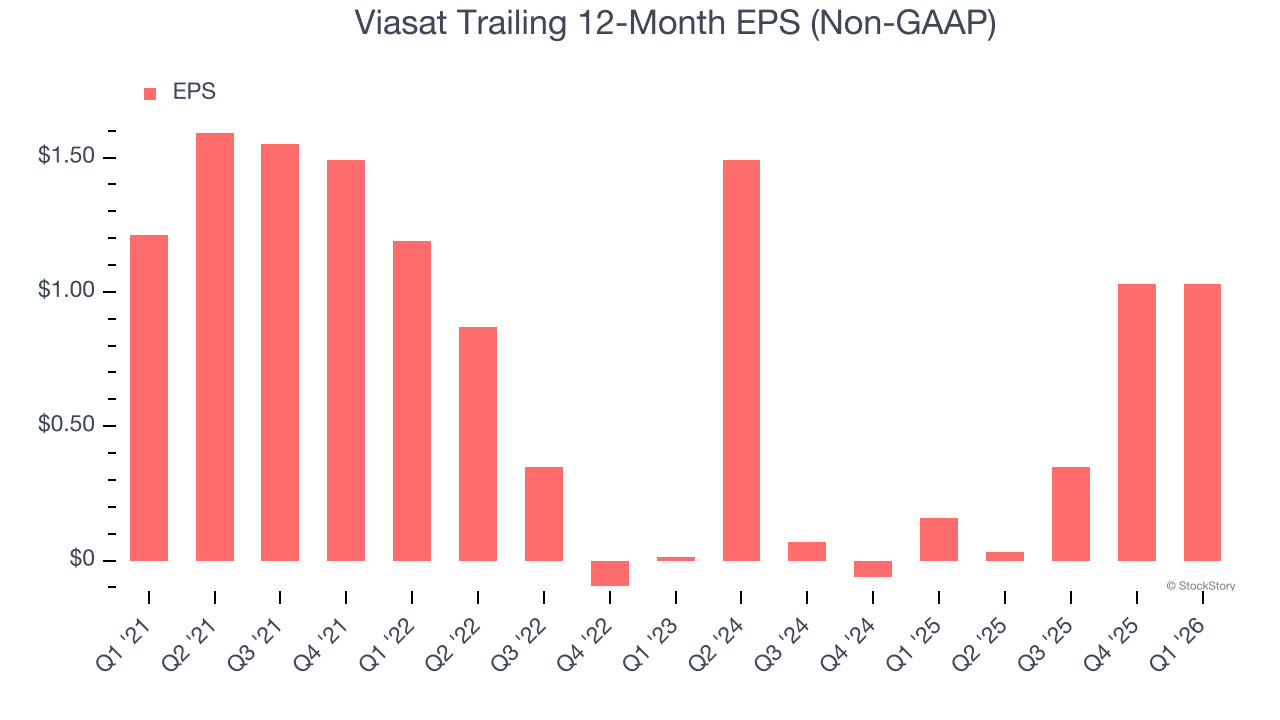

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Viasat, its EPS declined by 3.2% annually over the last five years while its revenue grew by 15.5%. This tells us the company became less profitable on a per-share basis as it expanded.

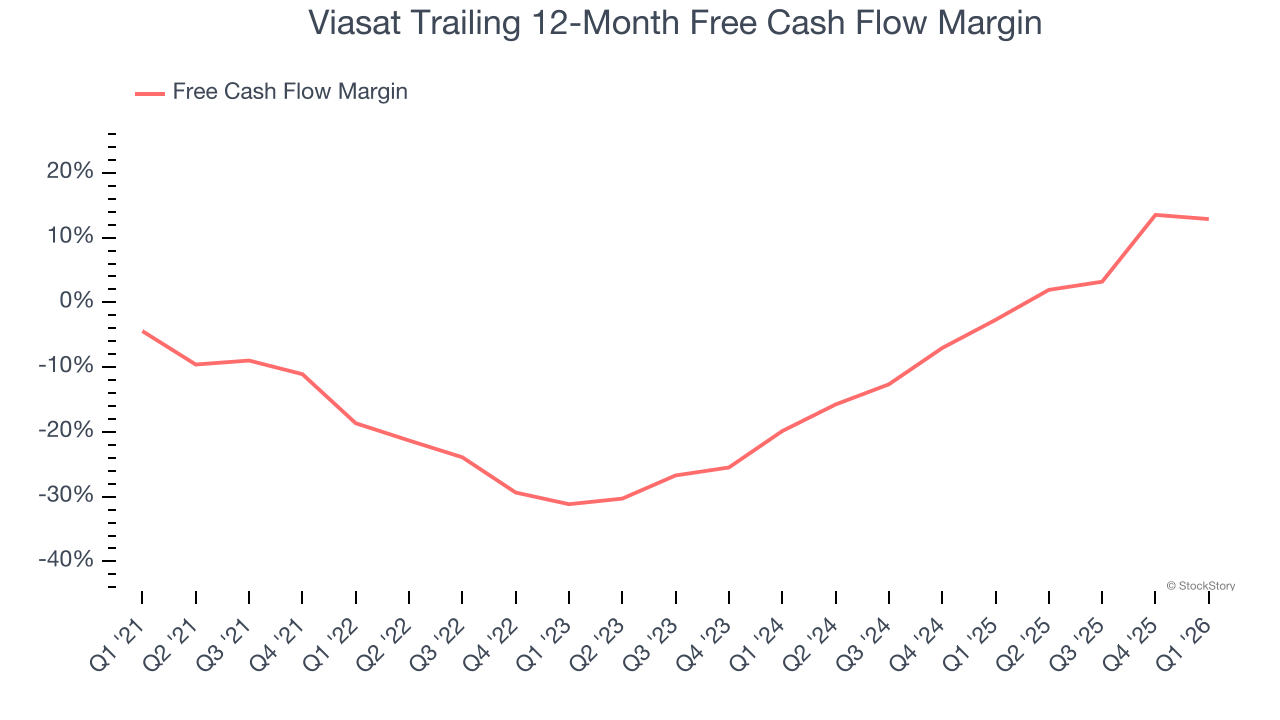

3. Cash Burn Ignites Concerns

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Viasat posted positive free cash flow this quarter, the broader story hasn’t been so clean. Viasat’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 8.9%, meaning it lit $8.91 of cash on fire for every $100 in revenue.

Final Judgment

Viasat isn’t a terrible business, but it isn’t one of our picks. After the recent surge, the stock trades at 193.5× forward P/E (or $62.46 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Viasat

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.